1099 Reporting Threshold Increases to $2,000 Beginning in 2026

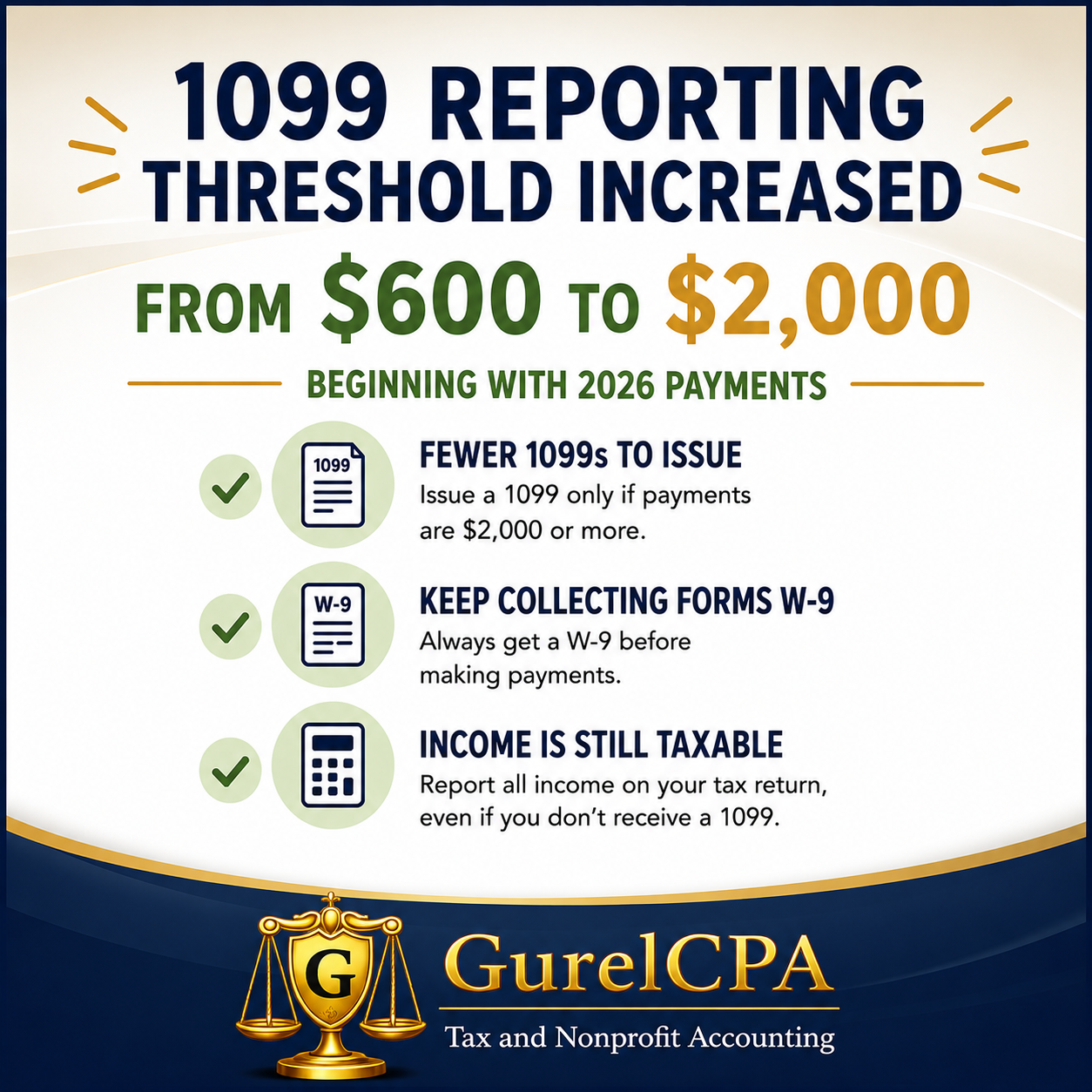

For years, taxpayers and businesses have been familiar with the $600 rule for issuing Forms 1099 to independent contractors and certain other payees. Beginning with payments made in 2026, that long-standing threshold has increased to $2,000 for Form 1099-NEC and some of the payments reported on Form 1099-MISC.

What Changed?

• 2025 and earlier: Form 1099 was issued if total qualifying payments were $600 or more.

• Beginning 2026, Form 1099 is required only if total qualifying payments are $2,000 or more.

•Beginning in 2027, the $2,000 threshold will be adjusted annually for inflation.

Businesses: Don't Stop Collecting Forms W-9

Although fewer businesses may need to issue 1099s, this is not a reason to stop collecting Forms W-9 from vendors. A contractor who receives only a few hundred dollars today may receive additional work later in the year that pushes total payments over the reporting threshold. Having a completed W-9 on file before making payments saves time and frustration later.

Individuals: Remember! Income Is Still Taxable

The higher reporting threshold does not change whether income is taxable. Contractors and self-employed individuals must still report all taxable income they receive, even if they never receive a Form 1099.

Watch for State Differences

The new $2,000 federal reporting threshold applies to payments beginning January 1, 2026. However, some states have their own information reporting rules and may continue using different thresholds until they update their laws or guidance. If you make payments to vendors in multiple states, be sure to verify each state's reporting requirements before year-end.

Need Help? Let’s Talk!

The new reporting rules may reduce paperwork for many businesses, but they also create new questions about who must receive a Form 1099 and when.

If you're unsure how these changes affect your business, we're happy to help you stay compliant while avoiding unnecessary filings. Contact GurelCPA for a free consultation.

This article is for informational purposes only and should not be relied upon as tax advice. Please contact me directly to discuss how this applies to your organization’s specific situation.