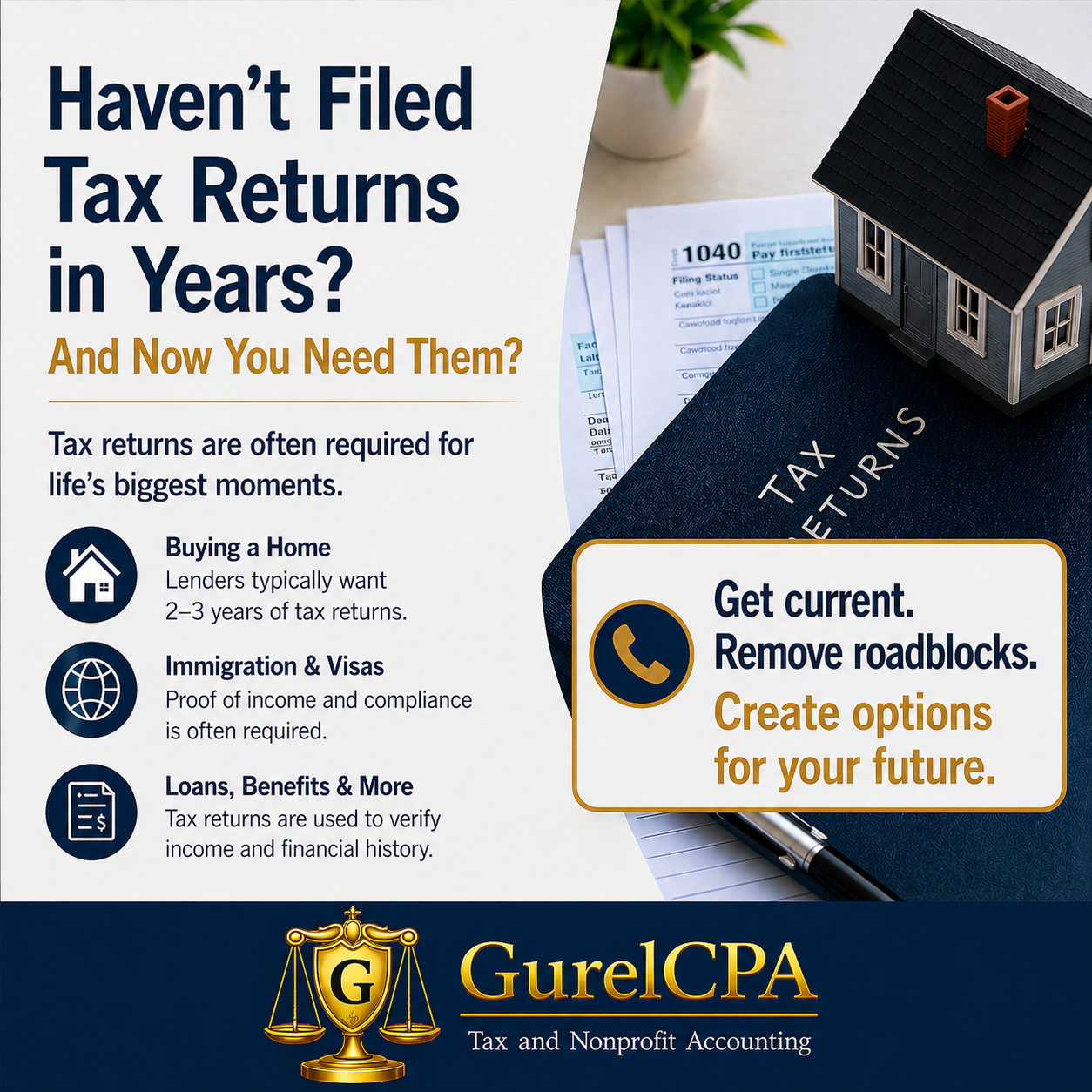

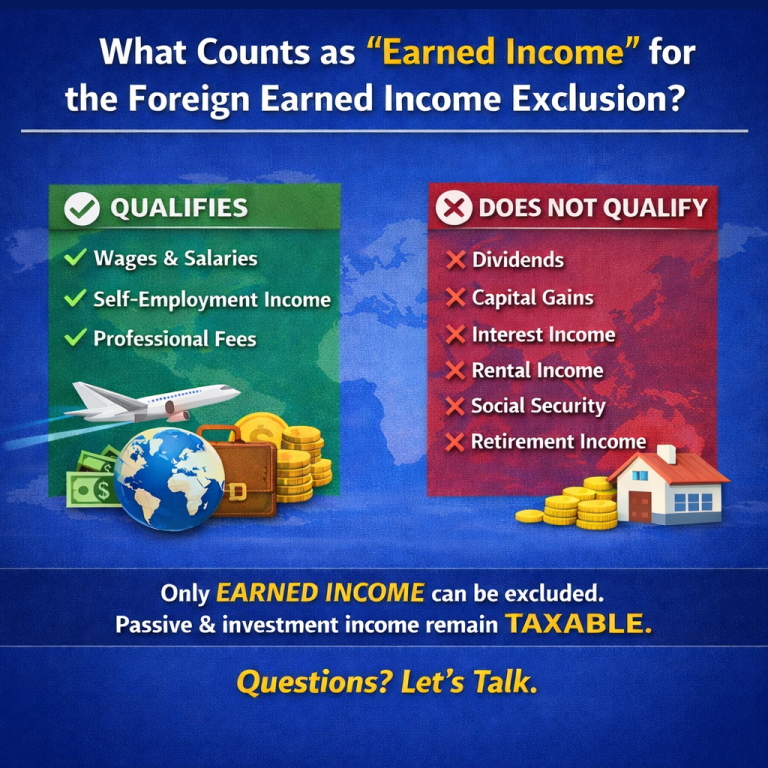

Do You Own an Interest in a Foreign Business?The IRS Wants to Know

Forms 5471 and 8865 can carry substantial penalties when overlooked.

Most people know they must report income earned outside the United States. What many do not realize is that simply owning an interest in a foreign business can create an IRS filing requirement, even if the business made little or no money.

Two of the most commonly overlooked international information returns are Form 5471 and Form 8865. These forms do not usually create additional tax by themselves, but failing to file them can result in substantial penalties.

Form 5471: Foreign Corporations

- Started a corporation outside the United States

- Own a significant percentage of a foreign corporation

- Became an officer or director under certain circumstances

- Have ownership in a controlled foreign corporation (CFC)

The form can require detailed ownership and financial information.

Form 8865: Foreign Partnerships

- Own an interest in a foreign partnership

- Control a foreign partnership

- Contribute significant property

- Meet ownership thresholds

Like Form 5471, Form 8865 requires detailed financial and ownership information.

The Penalties Can Be Severe

Failure to file can generally result in an initial $10,000 penalty per required form, with additional penalties possible if the failure continues.

International Reporting Is More Than Just FBARs

Foreign business ownership is a separate reporting requirement from FBAR and Form 8938.

Do Not Assume Someone Else Is Filing

These are U.S. information returns that are generally the responsibility of the U.S. taxpayer.

The Bottom Line

If you own, inherit, or invest in a foreign corporation or partnership, determine whether Forms 5471 or 8865 apply before filing your return.

The article is meant for informational purposes only. Please contact me directly to discuss how this applies to your individual tax situation.

The Hidden Home Insurance Rule?

It Could Cost You Thousands!

Many homeowners assume that as long as they have homeowners insurance, they are fully protected. Unfortunately, one little-known provision found in many homeowners policies can significantly reduce an insurance payout after a loss. It is commonly known as the 80% rule, and understanding it before you need it can save you thousands of dollars.

What Is the 80% Rule?

The 80% rule generally requires you to insure your home for at least 80% of its current replacement cost. Replacement cost is the amount it would take to rebuild your home using today's labor and material costs. It is not the same as your home's market value or your purchase price.

If your dwelling coverage falls below that threshold, your insurance company may reduce the amount it pays on a partial loss, even if the loss itself is well below your policy limit.

A Simple Example

Suppose your home's replacement cost is $600,000. Under the 80% rule, your policy should generally provide at least $480,000 of dwelling coverage.

If you carry only $400,000 of coverage and later suffer a $120,000 fire loss, your insurer may apply a coinsurance formula that reduces your reimbursement. Instead of paying the full covered loss (less any deductible), the insurance company may pay only a portion of it because the home was underinsured.

Why This Happens More Often Today

Over the past several years, construction costs have risen dramatically due to higher prices for lumber, concrete, roofing materials, electrical components, and skilled labor. A policy that provided adequate protection just a few years ago may no longer reflect today's rebuilding costs.

Many homeowners focus on the market value of their home, but insurers are concerned with reconstruction cost. In some areas, rebuilding can actually cost more than the home's current market value.

How to Protect Yourself

- Review your homeowners policy every year.

- Ask your insurance agent for an updated replacement-cost estimate.

- Notify your agent about major remodeling projects or additions.

- Consider whether an extended or guaranteed replacement-cost endorsement makes sense for your situation.

Don't Wait Until After a Loss

The worst time to discover you are underinsured is after your home has been damaged. A brief annual review can help ensure your coverage keeps pace with inflation and rising construction costs, reducing the chance of an unpleasant surprise during the claims process

The Bottom Line

The 80% rule is one of those insurance provisions that many homeowners have never heard of until it affects them. Spending a few minutes reviewing your policy today could help protect one of your largest financial investments tomorrow.

How Gurel CPA Can Help?

Although your insurance professional determines the appropriate level of coverage, understanding the financial consequences of being underinsured is an important part of protecting your overall financial plan. If you have questions about casualty losses, disaster-related tax issues, or other financial planning matters, Gurel CPA is here to help.

The article is meant for informational purposes only. Please contact me directly to discuss how this applies to your individual tax situation.

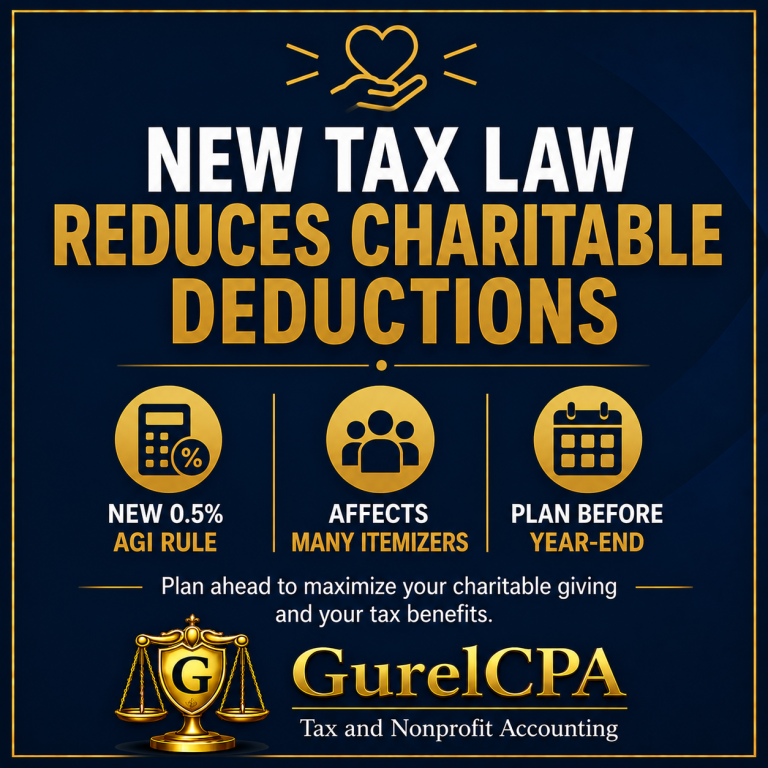

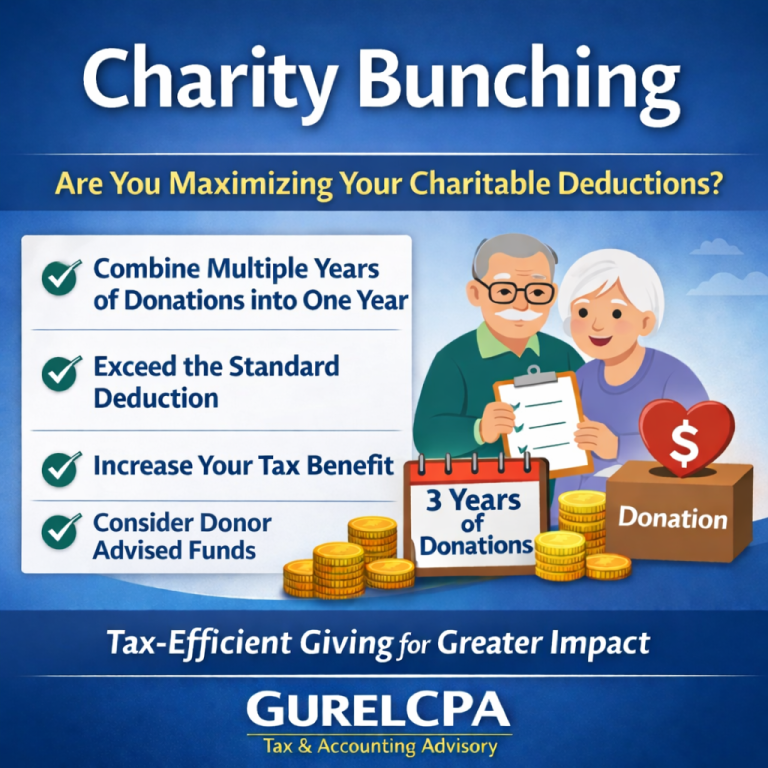

New Limits on Charitable Deductions

Starting with 2026 tax returns, many taxpayers who itemize deductions may receive a smaller charitable deduction than they expect.

A new tax law requires individuals who itemize to subtract 0.5% of Adjusted Gross Income (AGI) before claiming a charitable contribution deduction.

How the New Law Works

Beginning in 2026, only the portion of charitable contributions that exceeds 0.5% of your AGI is deductible. This creates a new threshold that reduces the deductible amount of many charitable gifts.

Example:

AGI: $200,000

• 0.5% of AGI = $1,000

• Charitable gifts = $5,000

• Deductible amount = $4,000

The first $1,000 of contributions is not deductible.

This Law Is Separate from Existing AGI Limits

Taxpayers may confuse the new 0.5% AGI floor with the long-standing limits on charitable deductions. They are different rules and both may apply.

• The new 0.5% AGI floor reduces the amount of contributions that can be deducted.

• The existing AGI percentage limits (such as the 60% of AGI limit for many cash gifts to public charities) continue to limit the maximum deduction that can be claimed.

In other words, itemizing taxpayers must first reduce their deduction by the new 0.5% floor, and then the remaining deduction is still subject to the applicable AGI limits.

Who Is Affected?

This change affects taxpayers who itemize deductions on Schedule A and make gifts to qualified charitable organizations. Taxpayers claiming the standard deduction are not subject to the 0.5% floor.

Why This Matters

Many generous donors will receive a smaller tax benefit than in prior years. Thoughtful year-end planning can help maximize the value of charitable giving.

Planning Opportunities

- Bunch several years of charitable gifts into one year.

- Donate appreciated securities instead of cash when appropriate.

- Use Qualified Charitable Distributions (QCDs) if you qualify.

- Coordinate charitable giving with your overall tax strategy.

Don't Let the New Law Surprise You

Charitable giving should always begin with supporting causes you care about, but understanding the new rules can help you receive every deduction available. If you expect to itemize deductions, review your charitable giving strategy before year-end.

Questions? Let’s Talk!

Contact GurelCPA. We can help you build a charitable giving strategy that supports both your favorite charities and your tax planning goals.

This article is provided for general informational purposes only and should not be considered tax advice. Each taxpayer’s situation is unique.

You Can Owe Tax on Money You Never Received

Most people assume they only pay income tax on money that actually lands in their bank account. Unfortunately, the tax law doesn't always work that way. You may owe federal income tax on income you never physically receive. These rules often surprise taxpayers and can create unexpected tax bills if they are not anticipated.

A Recent Tax Court Reminder

On July 14, 2026, the U.S. Tax Court issued its decision in Eiler v. Commissioner (167 T.C. No. 3). The taxpayers received a lawsuit settlement, but most of the settlement proceeds were paid directly to their attorneys under a contingent fee agreement.

The taxpayers argued that they should only be taxed on the amount they actually kept. The Tax Court disagreed. Relying on Commissioner v. Banks, the court held that when a lawsuit recovery is taxable, the taxpayer generally must include the entire recovery in income, including the portion paid directly to the attorney. Because the claims in this case did not qualify for a special deduction available for certain civil rights and employment cases, the attorney fees did not reduce taxable income.

The result was that the taxpayers owed tax on money they never personally received.

Other Situations Where This Can Happen

- Cancellation of Debt: When a lender forgives debt, the forgiven amount is generally taxable.

- Debt Settlements: Settling a loan or credit card for less than the balance may produce taxable cancellation-of-debt income and a Form 1099-C.

- Partnership and LLC Income: Owners are taxed on their share of business profits even if the business keeps the cash instead of distributing it.

- S Corporation Income: Shareholders generally pay tax on their share of corporate income whether or not cash distributions are made.

- Imputed Interest: The tax law sometimes treats interest as having been paid on below-market loans even when no interest actually changes hands.

- Foreclosures and Repossessions: Losing property can result in taxable gain, cancellation-of-debt income, or both depending on the facts.

Why These Rules Exist

The tax law often focuses on economic benefit rather than cash actually received. If your financial position improves because a debt disappears, a business earns income on your behalf, or another party satisfies an obligation you owe, the IRS may treat that benefit as taxable income.

Planning Can Prevent Costly Surprises

Many of these situations involve exceptions and planning opportunities. Understanding the tax consequences before signing a settlement, restructuring debt, or completing a transaction can help avoid unexpected tax bills.

How Can We Help?

Unexpected taxable income often catches taxpayers off guard because the transaction does not feel like income. If you are settling a lawsuit, negotiating debt, selling a business, or facing another complex financial transaction, Gurel CPA can help you understand the tax consequences before you make a costly decision.

The article is meant for informational purposes only. Please contact me directly to discuss how this applies to your individual tax situation.

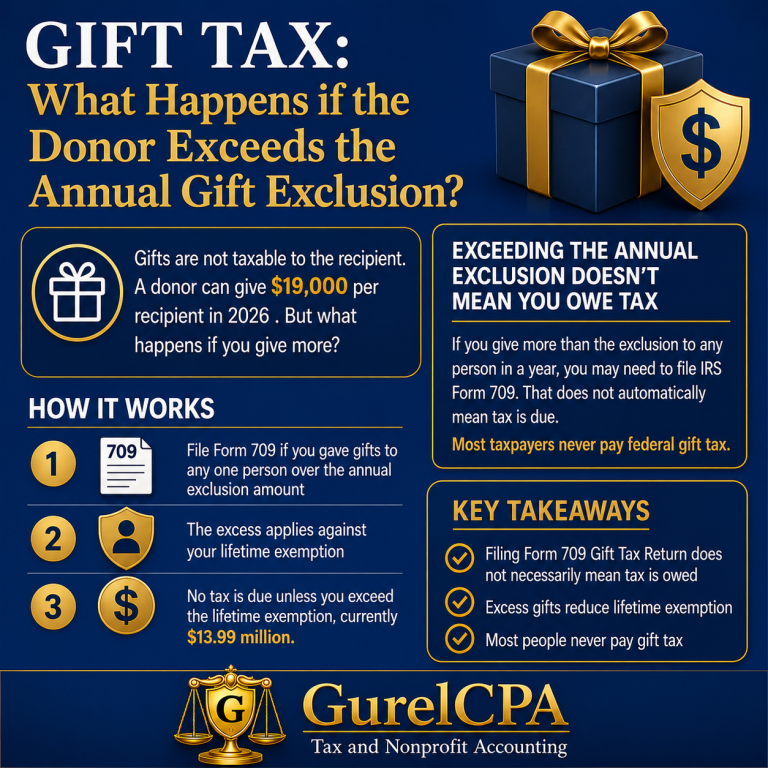

Gifting to a Non-U.S. Citizen Spouse?

Many married couples assume they can transfer unlimited amounts of money or property to each other without worrying about gift taxes.

While that's generally true when both spouses are U.S. citizens, the rules are different when one spouse is not a U.S. citizen.

Why Is There a Different Rule?

Normally, gifts between spouses qualify for the unlimited marital deduction. However, that unlimited deduction does not apply if the recipient spouse is not a U.S. citizen because assets could leave the U.S. transfer tax system. For 2026, the IRS has increased the annual tax-free gift limit for gifts to a non-U.S. citizen spouse to $194,000, up from $190,000 in 2025.

What Does the $194,000 Limit Mean?

You may give up to $194,000 to a non-U.S. citizen spouse during 2026 without creating a taxable gift. Larger gifts generally require Form 709 and reduce your lifetime exemption rather than immediately creating gift tax.

Examples:

Example 1: A $150,000 gift is fully covered by the annual exclusion.

Example 2: A $250,000 gift leaves $56,000 that generally uses part of the lifetime exemption and requires Form 709.

Estate Planning Opportunities

Making annual gifts within the exclusion can gradually transfer wealth while reducing future estate tax exposure. International families should coordinate gift, estate, and immigration planning.

Don't Confuse This With the Regular Gift Exclusion

For 2026:

- Annual gift exclusion to most individuals: $19,000

- Annual gift exclusion to a non-U.S. citizen spouse: $194,000

Bottom Line

If your spouse is not a U.S. citizen, don't assume the unlimited marital deduction applies. The higher 2026 exclusion provides additional planning opportunities, but larger gifts should be reviewed with a qualified tax advisor.

Questions about international tax planning or gift tax reporting? Contact GurelCPA to discuss your situation.

The article is meant for informational purposes only. Please contact me directly to discuss how this applies to your individual tax situation.

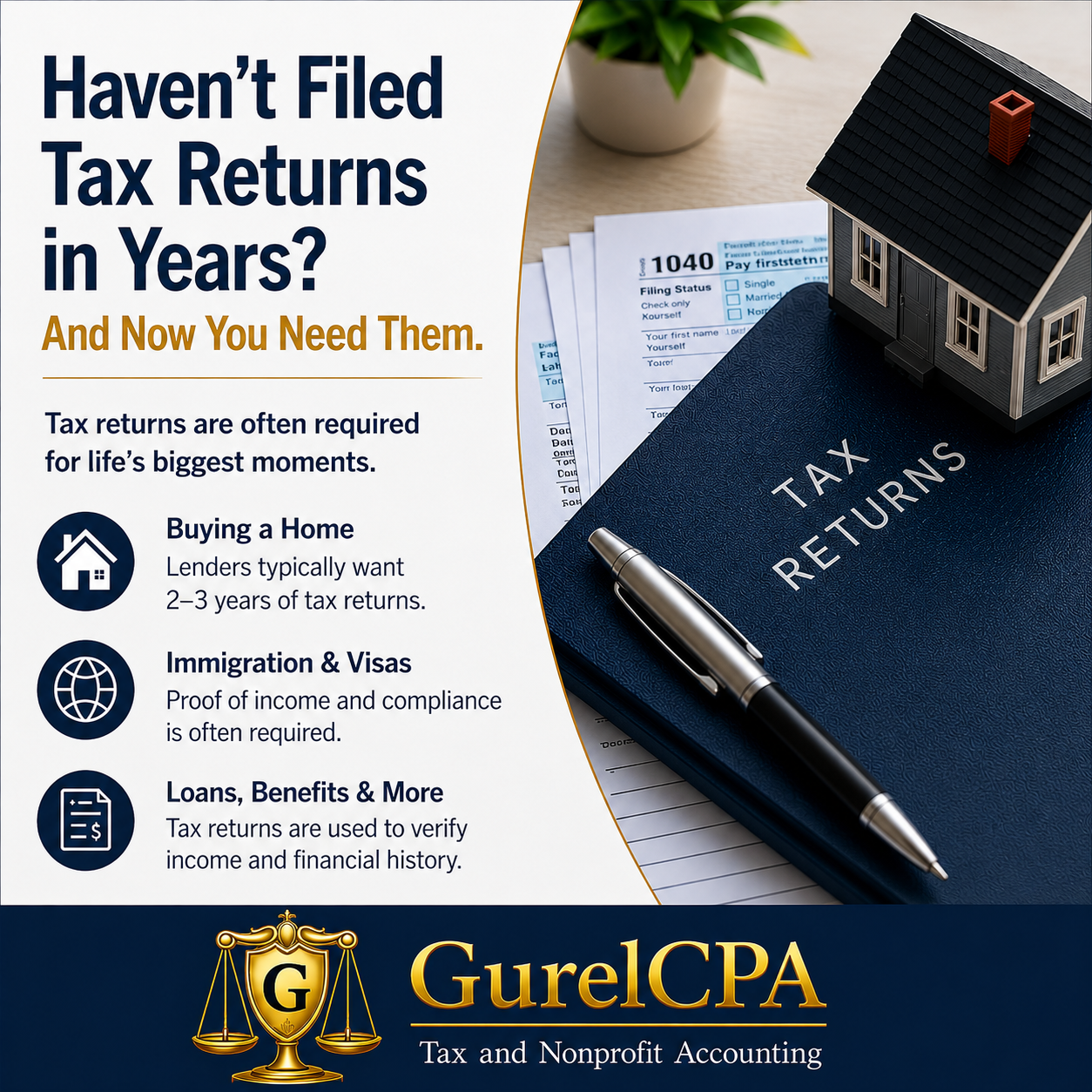

Hurricane and Wildfire Season Is Here: Are Your Tax Records Protected?

June marked the beginning of hurricane season in many parts of the United States and wildfire season in others.

While most people think about protecting their homes and families, it's equally important to protect the financial and tax records you may need after a disaster.

The IRS reminds taxpayers that a little preparation today can save significant stress and frustration later.

Start With Important Documents

- Tax returns

- Supporting tax documents

- Property records

- Insurance policies

- Estate planning documents

- Vehicle titles

- Business records

- Nonprofit financial records

Store digital copies securely in cloud storage or on an encrypted external drive kept in a separate location.

Take Photos of Valuable Property

- Furniture

- Electronics

- Appliances

- Artwork

- Jewelry

- Tools and equipment

- Business assets

These records may make it easier to support insurance claims and document losses if a disaster occurs.

Create and Maintain an IRS Online Account

- Tax transcripts

- Account balances

- IRS notices

- Payment history

- Filing information

If your paper records are lost, online access may help you obtain information needed to reconstruct your tax files.

Businesses and Nonprofits Should Take Extra Precautions

Business owners and nonprofit organizations should also protect accounting files, payroll records, vendor contracts, donor records, grant documentation, board minutes, and organizational documents. Cloud-based systems provide additional protection.

Tax Relief May Be Available After a Disaster

When a major disaster receives a federal disaster declaration, the IRS often provides extended filing deadlines, payment relief, and penalty relief. Taxpayers in designated disaster areas frequently receive this relief automatically.

Don't Wait Until Disaster Strikes

Taking a few hours now to organize records, back up documents, and document valuable property could save days or weeks of work later.

Need Help?

If you're unsure which tax and financial records should be retained or how long to keep them, contact me directly.

I offer a free consultation and can help you develop a recordkeeping system that protects your information and makes tax season easier.

This article is for informational purposes only and does not constitute tax advice. Every situation is different, especially when multiple years of unfiled returns are involved.

Don’t Give Them the House. Let Them Inherit It.

Many parents assume that giving a house to their children during their lifetime is a smart way to avoid probate or simplify their estate.

In reality, making a lifetime gift of appreciated real estate can create a significant tax problem for your children. In most cases, allowing your heirs to inherit the property instead of receiving it as a gift can save them tens or even hundreds of thousands of dollars in capital gains tax.

The Difference Is the Tax Basis

When you give someone a house during your lifetime, they generally receive your original tax basis in the property. This is called a carryover basis.

Example:

- You bought your home years ago for $150,000.

- Today it is worth $700,000.

- You give the house to your daughter.

Your daughter's tax basis is still $150,000. If she later sells the home for $700,000, she could owe capital gains tax on approximately $550,000 of gain, subject to any available exclusions.

What Happens If They Inherit the House?

When property is inherited, most assets receive a step-up in basis. The property's tax basis generally becomes its fair market value on the date of death (or an alternate valuation date if elected by the estate).

- Original purchase price: $150,000

- Value at death: $700,000

- Heir's new tax basis: approximately $700,000

If the property is sold shortly after inheritance for about that amount, there may be little or no taxable capital gain.

What About Probate?

Avoiding probate does not necessarily require giving away the property during your lifetime. Depending on your situation, alternatives may include:

- Revocable living trust

- Transfer-on-death deed (where available)

- Appropriate joint ownership arrangements

- Other estate planning techniques recommended by your attorney

Are There Exceptions?

Yes. There are situations where lifetime transfers make sense, including:

- Medicaid planning

- Asset protection planning

- Certain irrevocable trust strategies

- Other specialized estate planning situations

These decisions should always be made after considering both the legal and tax consequences.

The Bottom Line

One of the most expensive estate planning mistakes families make is giving appreciated real estate to children too soon. In many cases, allowing loved ones to inherit the property instead can provide a valuable step-up in basis and dramatically reduce future capital gains taxes.

Before transferring a home, vacation property, rental house, or other appreciated real estate, speak with both your CPA and your estate planning attorney. A simple planning decision today could save your family a substantial amount in taxes tomorrow.

Questions about gifting property or estate tax planning?

GurelCPA helps individuals and families understand the tax consequences of gifting, inheriting, and selling real estate so they can make informed financial decisions before transferring valuable assets.

The article is meant for informational purposes only. Please contact me directly to discuss how this applies to your individual tax situation.

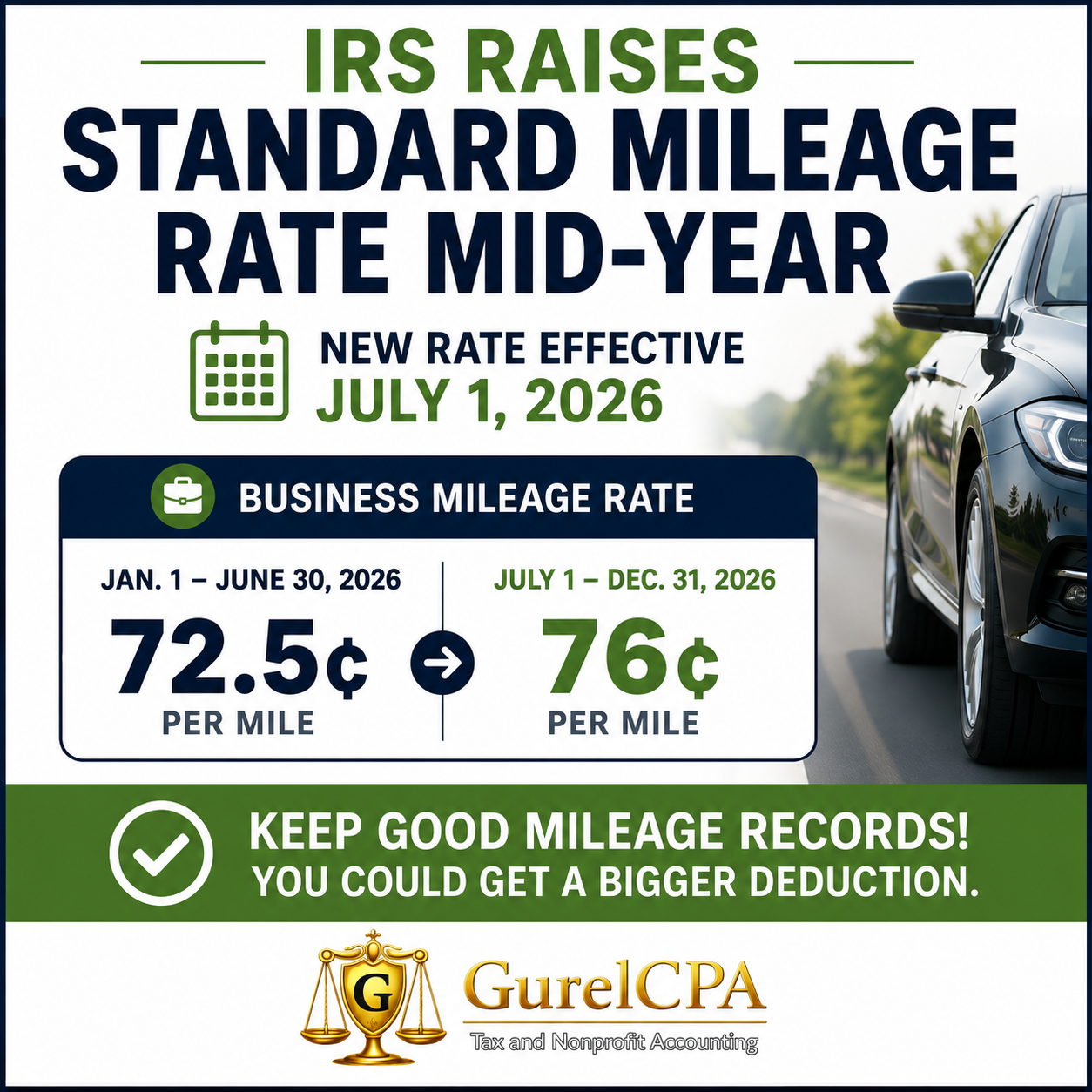

IRS Raises Standard Mileage Rates Mid-Year for 2026

Business Drivers Get a Bigger Deduction Beginning July 1

In an unusual mid-year move, the IRS has increased the optional standard mileage rates for the remainder of 2026 due to rising fuel costs. If you use your personal vehicle for business, medical, or certain moving purposes, this change could increase your tax deduction.

The new rates apply to miles driven on or after July 1, 2026.

New Standard Mileage Rates

For miles driven from January 1 through June 30, 2026, the standard mileage rates are:

- Business: 72.5 cents per mile

- Medical: 20.5 cents per mile

- Qualifying military moving: 20.5 cents per mile

- Charitable: 14 cents per mile

For miles driven on or after July 1, 2026, the rates are:

- Business: 76 cents per mile

- Medical: 23.5 cents per mile

- Qualifying military moving: 23.5 cents per mile

- Charitable: 14 cents per mile (unchanged)

Moving expenses are deductible only for qualifying active-duty members of the U.S. Armed Forces and certain members of the intelligence community.

Who Benefits?

- Self-employed individuals

- Independent contractors

- Gig workers (Uber, Lyft, DoorDash, Instacart, etc.)

- Sole proprietors

- Farmers

- Small business owners who use their personal vehicles for business

Keep Good Mileage Records

Because the rate changed in the middle of the year, you'll need to separate your mileage into two periods:

- Miles driven January 1 through June 30

- Miles driven July 1 through December 31

Standard Mileage vs. Actual Expenses

The standard mileage rate is optional. Some taxpayers may receive a larger deduction by deducting their actual vehicle expenses instead. Actual expenses can include:

- Gas and oil

- Repairs and maintenance

- Tires

- Insurance

- Registration fees

- Depreciation (subject to IRS rules)

A Rare Mid-Year Change

The IRS normally announces one mileage rate each fall for the following calendar year. Mid-year adjustments are uncommon and generally occur only when fuel prices change dramatically. The last mid-year increase occurred in 2022.

Bottom Line

If you drive for business, be sure your mileage records reflect the new rates beginning July 1st. Even a few thousand business miles can produce a meaningful additional deduction.

If you have questions about deducting vehicle expenses or would like help determining whether the standard mileage method or actual expenses will save you more tax, contact GurelCPA. We're here to help you keep more of what you earn.

This article is for informational purposes only and should not be relied upon as tax advice. Please contact me directly to discuss how this applies to your individual tax situation.

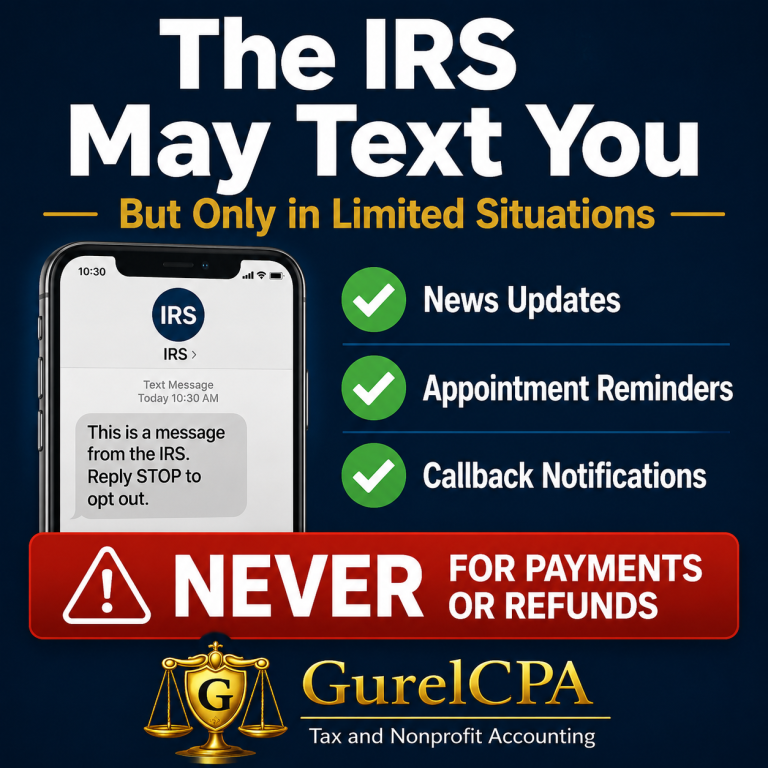

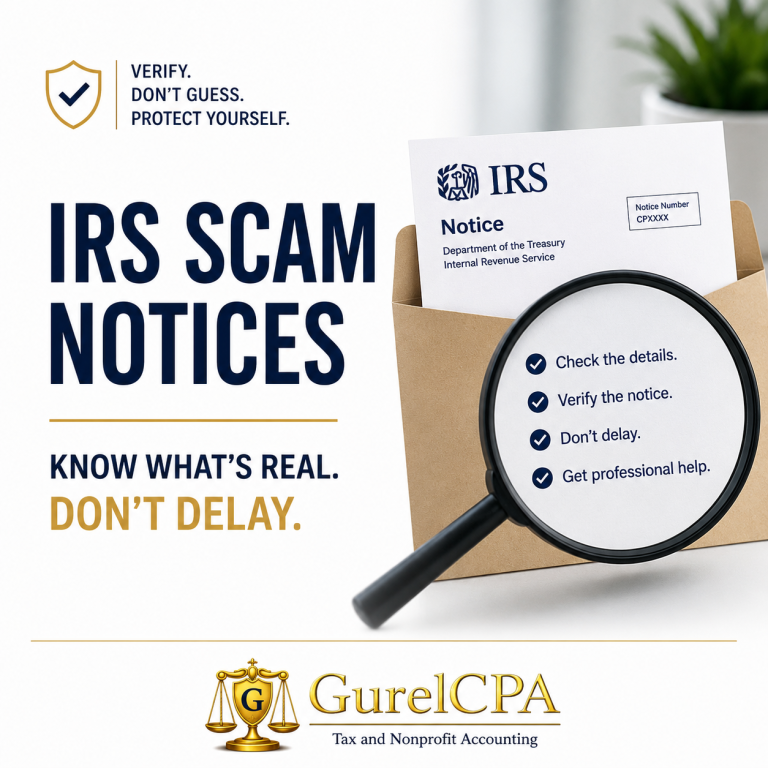

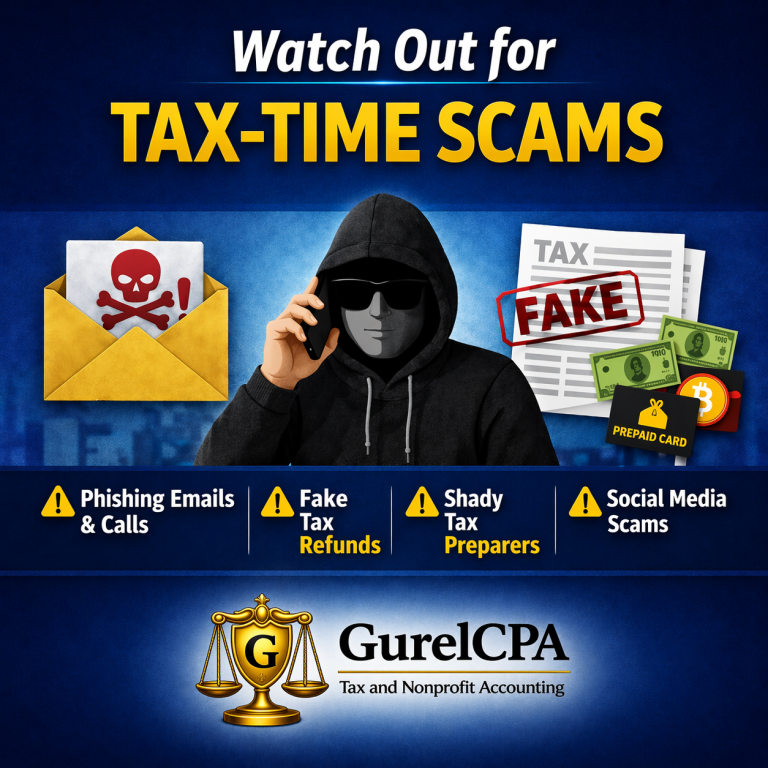

The IRS May Text You... But Here's How to Know if It's Real

For years, taxpayers have been told one simple rule:

"The IRS will never text you."

That advice was accurate for many years. Today, however, it's no longer true.

The IRS has expanded its digital services and now sends certain text messages to taxpayers who have opted in to receive them. The change is intended to improve customer service, but it also gives scammers another opportunity to confuse taxpayers.

Here's what you need to know.

When the IRS May Send a Text

The IRS now uses text messaging for a limited number of situations, including:

IRS News and Updates

If you've signed up to receive IRS news and announcements, you may receive text notifications about:

• Tax law changes

• IRS Newswire updates

• Account notifications

• Security verification codes

These messages are optional and require you to subscribe first.

IRS Appointment Reminders

If you've scheduled an appointment at an IRS Taxpayer Assistance Center and choose to receive text updates, the IRS may send reminders or let you know when it's your turn to be seen.

IRS Callback Notifications

Instead of waiting on hold, some IRS phone services now offer a callback option. If you request one, the IRS may text you when an agent is preparing to return your call.

The IRS Still Will NOT Text You About These Things

The IRS will never send an unexpected text asking you to:

• Pay taxes immediately

• Click a link to claim a refund

• Provide your Social Security number

• Verify your banking information

• Send passwords or security codes

• Scan a QR code to avoid penalties

If a message does any of these things, it's almost certainly a scam.

Watch for IRS Short Codes

Legitimate IRS text messages come from official short code numbers rather than ordinary 10-digit phone numbers.

Current IRS short codes include:

• 91040 – IRS news, appointment reminders, account notifications, and security codes

• 34381 – IRS callback notifications

Even so, scammers continue to get more sophisticated. Never assume a message is legitimate simply because it appears professional.

One Important Security Tip

If you receive a text containing a security code that you didn't request, don't ignore it. It may mean someone is attempting to access your IRS Online Account.

Never give that code to anyone. Instead, log directly into your IRS Online Account yourself and review your account activity.

What To Do if You Receive a Suspicious IRS Text

• Don't click any links.

• Don't reply.

• Don't provide personal information.

• Take a screenshot if possible.

• Forward the message to phishing@irs.gov.

• Forward the text to 7726 (SPAM).

• Delete the message afterward.

Bottom Line

IRS communication is gradually becoming more digital, but scammers are evolving just as quickly.

A legitimate IRS text will only be sent in limited situations that you initiated or specifically agreed to receive. If a text unexpectedly demands money, personal information, or immediate action, treat it as a scam until proven otherwise.

If you're ever unsure whether an IRS message is legitimate, contact GurelCPA before responding. A few minutes of caution can prevent identity theft and costly fraud.

The article is meant for informational purposes only. Please contact me directly to discuss how this applies to your individual tax situation.

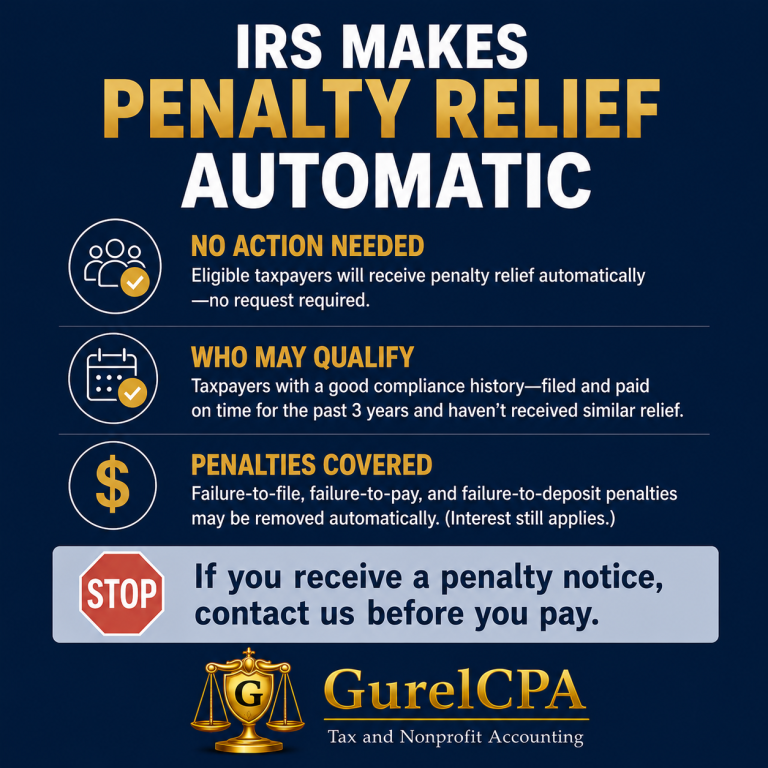

IRS Makes Penalty Relief Automatic for Many Taxpayers

The IRS has announced a significant taxpayer-friendly change that will make it easier for eligible individuals and businesses to avoid certain IRS penalties. Instead of requiring taxpayers to request relief, the IRS will begin granting qualifying penalty relief automatically to taxpayers with a strong history of compliance.

What's Changing?

For many years, taxpayers who qualified for First Time Abate (FTA) penalty relief had to know the program existed and contact the IRS to request it. Many eligible taxpayers never received this relief simply because they didn't know to ask.

The IRS is replacing that process with a new system called Automatic Exemption from Penalty (AEP).

Under AEP, the IRS will determine eligibility during return processing and automatically remove qualifying penalties without requiring taxpayers to file a request or make a phone call.

Who May Qualify?

- Filing required tax returns on time for the previous three years.

- Paying tax due on time (or making appropriate payment arrangements).

- Not having received similar administrative penalty relief during the look-back period.

Which Penalties Are Covered?

- Failure-to-File penalties

- Failure-to-Pay penalties

- Failure-to-Deposit penalties (primarily for businesses)

Interest on unpaid taxes still applies, and taxpayers remain responsible for paying any tax owed.

When Does It Begin?

The IRS is beginning the transition during the summer of 2026.

• 2025 tax year returns and 2026 quarterly business returns are part of the transition period. Some eligible taxpayers may still receive penalty notices during this phase. If that happens, qualifying taxpayers can still request First Time Abate under the existing rules.

• For returns with original due dates on or after January 1, 2027, AEP is expected to replace First Time Abate for eligible taxpayers, making the relief automatic.

If You Don't Qualify

Taxpayers who don't meet the requirements for AEP may still request penalty relief based on reasonable cause, such as serious illness, natural disasters, or other circumstances beyond their control. The IRS will continue reviewing those requests individually.

Why This Matters

This change removes one of the biggest frustrations in the penalty relief process. Previously, taxpayers often needed to know about the First Time Abate program or hire a tax professional to request it. Under the new system, many eligible taxpayers will receive the relief automatically, reducing paperwork, phone calls, and unnecessary penalties.

Need Help?

If you've received an IRS penalty notice, don't assume you must pay it. You may qualify for automatic relief or another form of penalty abatement. Before paying an IRS penalty, it's worth having the notice reviewed to determine whether relief is available.

The article is meant for informational purposes only. Please contact me directly to discuss how this applies to your individual tax situation.

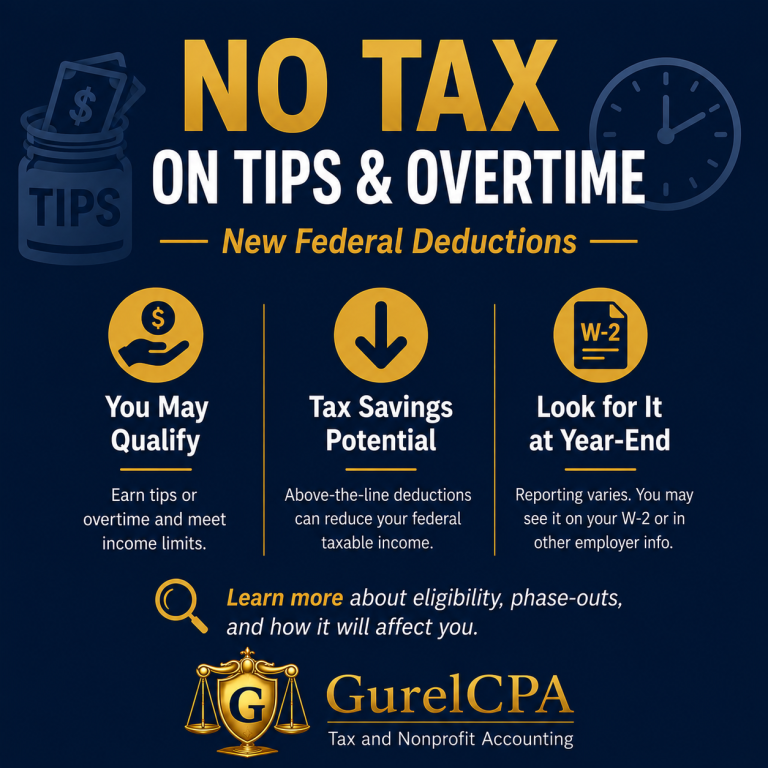

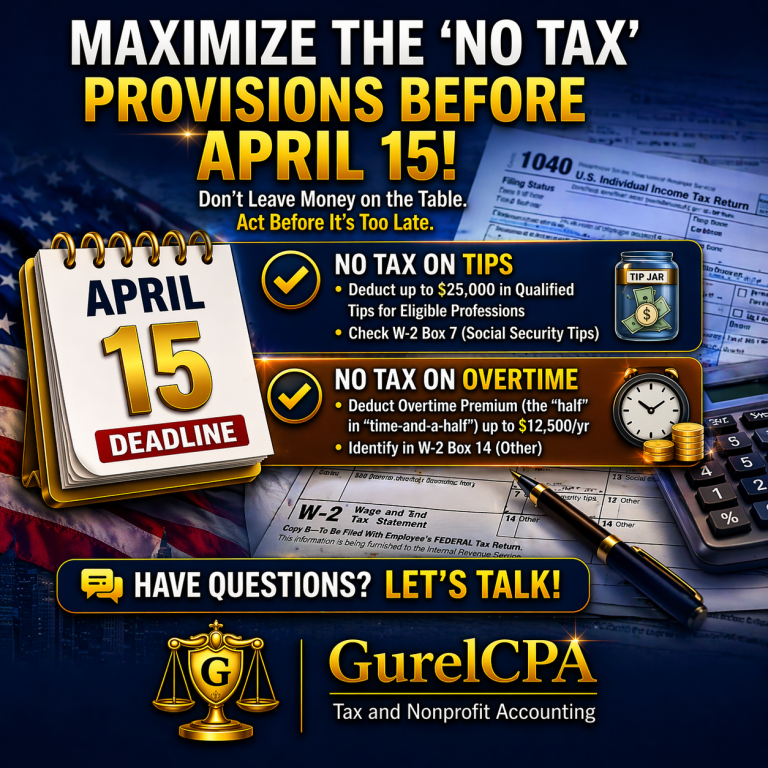

No Tax on Tips and Overtime: What Workers Need to Know

Millions of American workers may qualify for new federal tax deductions for tips and overtime beginning with the 2025 tax year.

Although these provisions are often called “No Tax on Tips” and “No Tax on Overtime,” the name is a little misleading. The income is still taxable, but eligible workers may be able to claim a deduction that reduces their federal taxable income when they file their tax return. These deductions are currently scheduled to apply for tax years 2025 through 2028.

Who May Qualify?

You may benefit if you receive:

- Qualified tips in an occupation that customarily and regularly receives tips.

- Qualified overtime compensation required under federal overtime rules.

- Income below the phase-out thresholds.

The deductions begin to phase out when modified adjusted gross income exceeds $150,000 for most individual filers and $300,000 for married couples filing jointly.

This Isn't a Tax-Free Paycheck

Many people expected these rules to eliminate taxes from each paycheck. That isn't how they work.

- Federal income tax may still be withheld.

- Social Security and Medicare (FICA) taxes still apply.

- State income taxes may still apply, depending on your state.

Instead, you'll generally claim the deduction when you file your federal tax return, which could reduce the tax you owe or increase your refund.

How Will It Show Up at Year-End?

For the 2025 tax year, employers were given transition relief. That means not every employer will report qualified tips or qualified overtime the same way. You may receive the information:

- On your Form W-2.

- In Box 14 of your W-2.

- On a separate employer statement.

- Through your employer's payroll portal.

Don't assume that if you don't see a special code on your W-2 you aren't eligible. Keep your year-end payroll information with your tax records.

What Should You Do Now?

- Save your year-end payroll documents.

- Review your W-2 carefully when it arrives.

- Make sure your tax preparer knows you received qualifying tips or overtime.

- Ask questions if your employer's reporting isn't clear.

The IRS continues to issue guidance, and reporting should become more standardized in future years.

The Bottom Line

These new deductions could reduce your federal income tax if you qualify, but they are not automatic paycheck exemptions and they don't eliminate payroll taxes.

The most important thing is making sure your year-end tax documents accurately reflect your qualifying tips or overtime so you receive every deduction you're entitled to.

Questions? Let’s Talk!

If you have questions about whether you qualify or how these new deductions apply to your situation, I'd be happy to help.

This article is provided for general informational purposes only and should not be considered tax advice. Each taxpayer’s situation is unique.

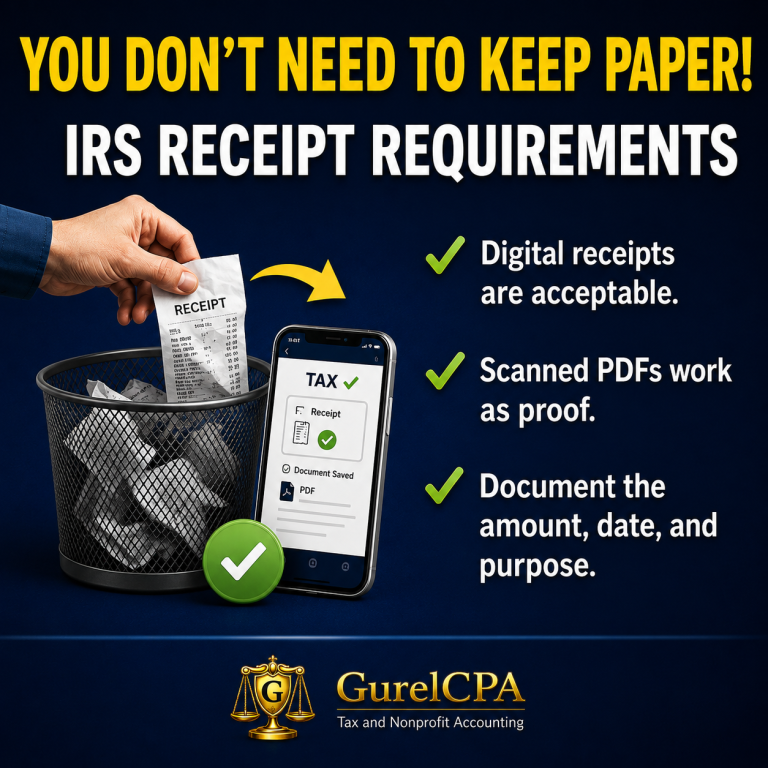

You Don't Need to Keep Paper Receipts

Many taxpayers think the IRS requires a receipt for every deduction. That is not exactly the rule.

The real rule is this: if you claim a deduction, credit, or business expense, you must be able to substantiate it. In plain English, you need records that show what you spent, when you spent it, and why it was deductible.

What does “substantiate” mean?

To substantiate an expense means you can support it with records. Depending on the item, that may include a receipt, invoice, canceled check, bank or credit card statement, mileage log, charitable acknowledgment, or other documentation.

But a bank or credit card statement alone is often not enough. It may show that money was spent, but not exactly what was purchased or whether it was deductible.

Do you always need a receipt?

Not always in the narrowest technical sense, but in practice, keeping the receipt is usually the safest approach.

If you want to deduct an expense, keep the receipt and any related backup that helps explain it. A store receipt may show what was purchased, while a credit card statement may only show the total charge.

Why receipts matter

Receipts and supporting records help in three ways.

- They help you prepare an accurate return.

- They help your tax preparer determine what is and is not deductible.

- They protect you if the IRS questions the return later.

If the IRS examines your return and you cannot support a deduction, the deduction may be denied even if you really did spend the money.

Some categories need especially strong documentation:

Business meals and travel

Business meals and travel are areas where taxpayers often run into trouble. You should keep records showing the amount, date, place, and business purpose of the expense. For meals, it is also helpful to note who was involved.

Vehicle expenses and mileage

If you claim business mileage, you should keep a contemporaneous mileage log showing the date, destination, business purpose, and miles driven. Reconstructing mileage later is much weaker.

Charitable contributions

For charitable deductions, the rules are stricter than many people realize.

For any single contribution of $250 or more, you generally need a contemporaneous written acknowledgment from the charity.

For smaller donations, a bank record, receipt, or written communication from the organization may be enough, depending on the facts.

What about the “under $75” rule?

Many taxpayers have heard that receipts are not required for amounts under $75. That idea is often misunderstood.

There are limited exceptions in certain situations, but taxpayers should not treat “under $75” as a general rule for undocumented deductions. As a practical matter, if you are claiming it, keep the record.

Are digital receipts acceptable?

Yes. Digital records are acceptable.

Scanned receipts, PDF invoices, emailed confirmations, bookkeeping software records, and organized electronic files are all fine as long as they are legible, accurate, and accessible.

You do not have to keep boxes of paper if you have a reliable digital system.

How long should taxpayers keep receipt records?

A common rule of thumb is at least three years after the return is filed. Some records should be kept longer.

If the records relate to property basis, depreciation, investments, or other items that affect future returns, keep them as long as they remain relevant, plus the applicable retention period after the item is sold or disposed of.

What happens if you do not have receipts?

If you cannot substantiate a deduction, the IRS may disallow it. That can lead to additional tax, penalties, interest, and stress.

Good recordkeeping is not just paperwork. It is part of protecting the deduction itself.

Practical advice for taxpayers

The easiest approach is to use a simple system and stay consistent.

- Save receipts when the purchase happens.

- Use a separate business bank account or credit card for business activity.

- Scan or photograph paper receipts.

- Keep digital folders by year and category.

- Make notes about business purpose while the details are still fresh.

- Maintain mileage logs in real time.

Final thoughts

IRS receipt requirements are really about proof.

The question is not just whether you spent the money. The question is whether you can show that the expense was legitimate, deductible, and properly reported.

Good records make tax preparation easier, reduce audit risk, and put you in a stronger position if the IRS ever asks questions.

Questions? Let’s Talk

At GurelCPA.com, I help taxpayers and business owners not only file accurate returns, but also build practical recordkeeping habits that support those returns.

This article is for informational purposes only and does not constitute legal, tax, or accounting advice for your specific situation. Tax rules can vary based on the facts and circumstances involved. Please contact me directly to discuss your situation and schedule a free consultation.

Are You Happy With Your CPA?

That is the Question I Ask Prospective Clients

If the Answer is Yes:

That’s something to value. A strong CPA relationship is built on trust, communication, and long-term understanding — and if you’ve found that, you’re fortunate to have a true trusted advisor.

If the Answer is No:

Then it’s probably worth a conversation. Feeling unheard, rushed, or misunderstood financially is often a sign that a better professional fit may exist.

And for some people, the honest answer is:

“I don’t have a CPA.”

Where CPA Services Truly Add Value

There are specific situations where professional guidance can create real financial value and prevent costly mistakes — especially when complexity increases.

This commonly includes small business ownership (entity structure, expense classification, tax strategy, cash flow planning, estimated taxes, and compliance obligations) and rental properties or real estate (depreciation strategy, passive activity rules, loss limitations, capital gains planning, and long-term tax structuring)

When You May Not Need a CPA

Not everyone needs a CPA.

If your financial life is simple — for example, if all of your income comes from W-2 wages, investment accounts, and basic sources of income — there are reliable, user-friendly tax software platforms that many people can use successfully on their own.

A Different Kind of CPA Relationship

My approach to accounting isn’t transactional — it’s relational. It’s about understanding your life, your business, and your goals — not just preparing returns.

If you’re happy with your CPA, that’s something to value.

If you’re not, we should talk.

If you don’t have one — and your financial life is becoming more complex — it may be time to explore whether having a trusted advisor could make a meaningful difference.

Question? Let’s Talk!

A core principle of my practice has always been empowerment: helping people understand their finances and supporting them in doing for themselves what they feel comfortable doing.

Contact GurelCPA for a free consultation today!

The article is meant for informational purposes only. Please contact me directly to discuss how this applies to your individual tax situation.

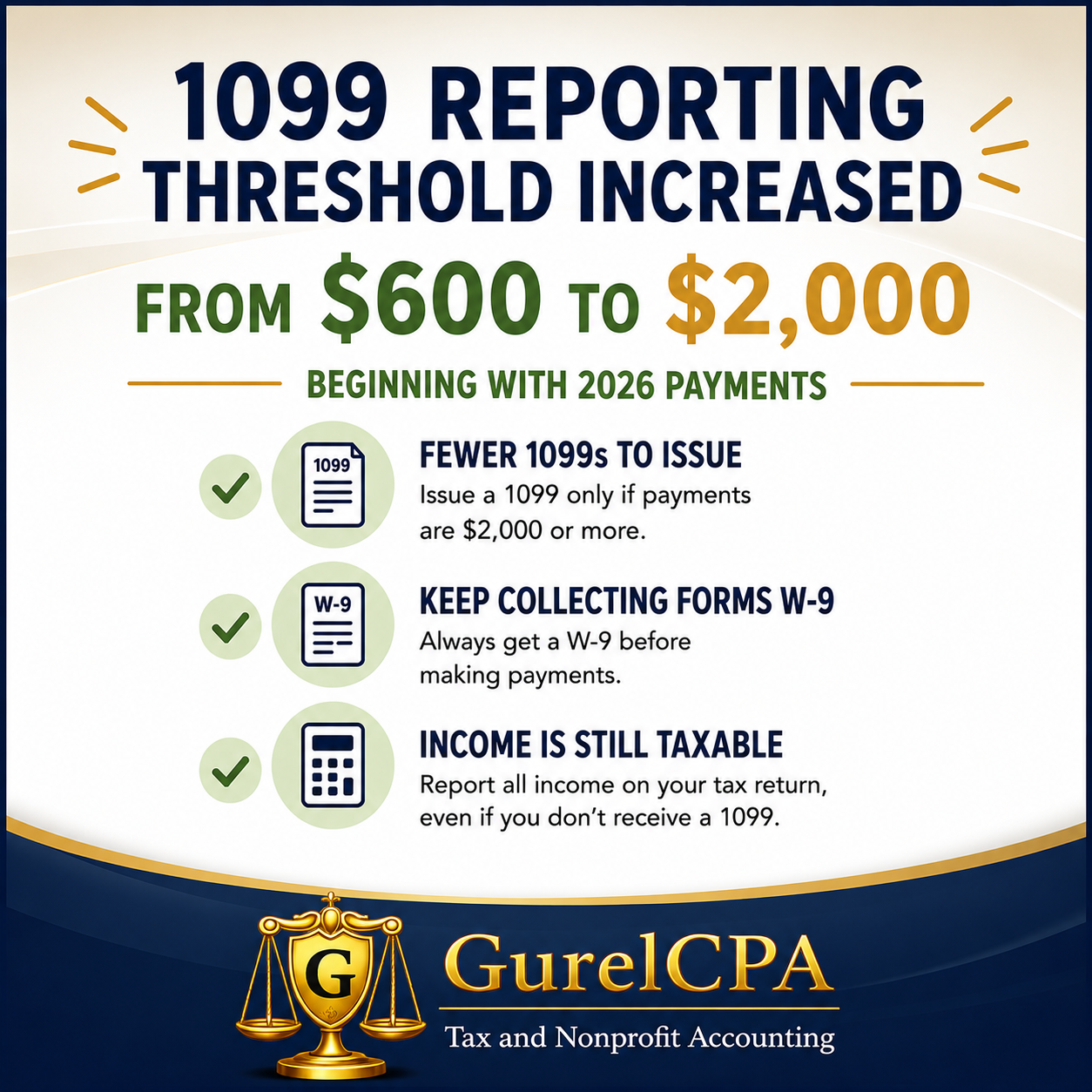

1099 Reporting Threshold Increases to $2,000 Beginning in 2026

For years, taxpayers and businesses have been familiar with the $600 rule for issuing Forms 1099 to independent contractors and certain other payees. Beginning with payments made in 2026, that long-standing threshold has increased to $2,000 for Form 1099-NEC and some of the payments reported on Form 1099-MISC.

What Changed?

• 2025 and earlier: Form 1099 was issued if total qualifying payments were $600 or more.

• Beginning 2026, Form 1099 is required only if total qualifying payments are $2,000 or more.

•Beginning in 2027, the $2,000 threshold will be adjusted annually for inflation.

Businesses: Don't Stop Collecting Forms W-9

Although fewer businesses may need to issue 1099s, this is not a reason to stop collecting Forms W-9 from vendors. A contractor who receives only a few hundred dollars today may receive additional work later in the year that pushes total payments over the reporting threshold. Having a completed W-9 on file before making payments saves time and frustration later.

Individuals: Remember! Income Is Still Taxable

The higher reporting threshold does not change whether income is taxable. Contractors and self-employed individuals must still report all taxable income they receive, even if they never receive a Form 1099.

Watch for State Differences

The new $2,000 federal reporting threshold applies to payments beginning January 1, 2026. However, some states have their own information reporting rules and may continue using different thresholds until they update their laws or guidance. If you make payments to vendors in multiple states, be sure to verify each state's reporting requirements before year-end.

Need Help? Let’s Talk!

The new reporting rules may reduce paperwork for many businesses, but they also create new questions about who must receive a Form 1099 and when.

If you're unsure how these changes affect your business, we're happy to help you stay compliant while avoiding unnecessary filings. Contact GurelCPA for a free consultation.

This article is for informational purposes only and should not be relied upon as tax advice. Please contact me directly to discuss how this applies to your organization’s specific situation.

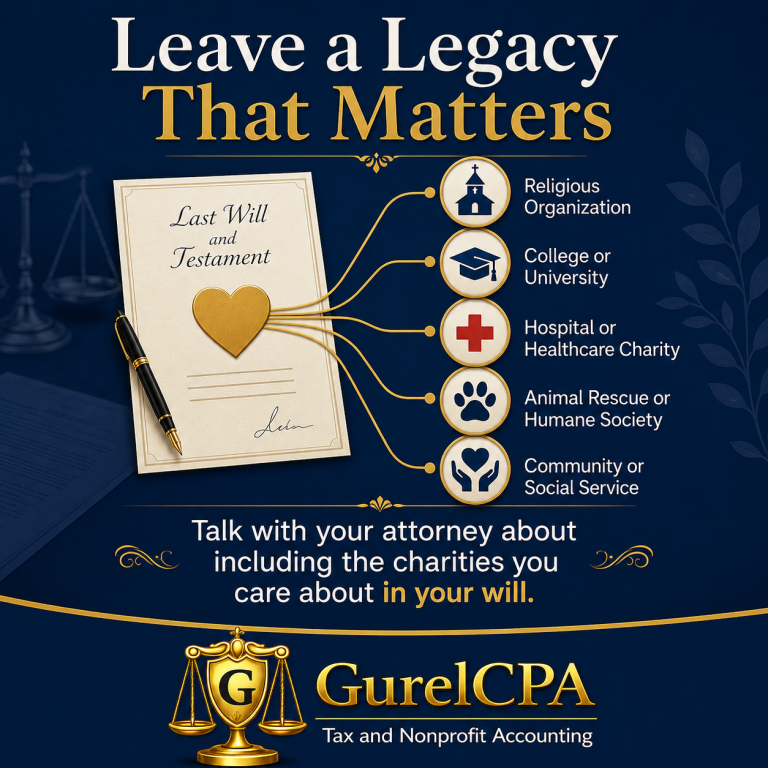

Leave a Legacy That Matters

Creating a will is one of the most important financial and personal decisions you'll make. It allows you to decide how your property will be distributed, who will carry out your wishes, and how you want to be remembered.

Most people naturally think first about providing for a spouse, children, or other loved ones. That's exactly what a will should do. But while you're meeting with your attorney, there is another important conversation to have.

What are the charitable organizations that have made a difference in your life?

Including a charitable gift in your will allows you to continue supporting the causes that have been meaningful to you throughout your life. Your gift does not have to be large. Even a modest bequest can make a lasting difference.

You may have several organizations that reflect your values and have earned your support over the years, such as:

- Your church or other religious organization

- A college or university

- A hospital or healthcare charity

- An animal rescue or humane society

- A food bank or other community service organization

Think about the organizations that have helped shape your life. Perhaps your church has been an important part of your family's story. Maybe a college or university opened doors to your career. A hospital may have provided exceptional care to someone you love, or a local nonprofit may have strengthened your community. These organizations often leave a lasting impression, and your will can allow you to continue supporting their mission.

A Few Practical Suggestions

- Make a list of the organizations that are important to you.

- Use each charity's correct legal name so there is no confusion.

- Review your will every few years, especially after major life events.

- Let your family know why these organizations are meaningful to you.

A charitable bequest does not have to be a large percentage of your estate. Some people leave a specific dollar amount, while others leave a percentage of what remains after family members have been provided for. Your attorney can help determine the approach that best fits your goals.

If you are creating or updating your will, take a few minutes to make a list of the charities that have been important to you. Share that list with your attorney and discuss whether including one or more charitable gifts makes sense as part of your estate plan. Your attorney can prepare the legal documents.

As Your CPA:

I can help you understand the tax considerations of charitable giving as part of your overall estate and financial plan. In some situations, charitable giving may have income tax or estate planning implications, particularly when retirement accounts or appreciated assets are involved. Working together, your attorney and CPA can help ensure your wishes are carried out efficiently.

Bequests do not have to be large to make an impact

Your will is more than a legal document. It is an opportunity to leave a legacy that reflects both the people and the causes that mattered most to you.

Question? Let’s Talk!

If you have questions about the tax aspects of charitable giving or would like to discuss how it fits into your overall financial plan, contact GurelCPA for a free consultation.

The article is meant for informational purposes only. Please contact me directly to discuss how this applies to your individual tax situation.

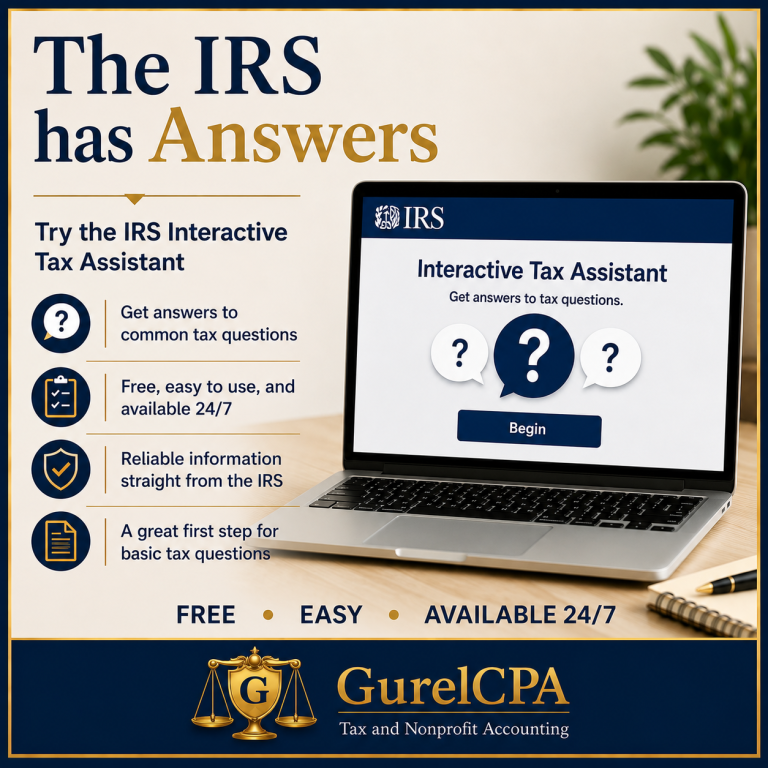

IRS Interactive Tax Assistant: Get Answers to Common Tax Questions

Did you know the IRS offers a free online tool that can answer many common tax questions?

The IRS Interactive Tax Assistant (ITA) asks you a series of simple questions and provides answers based on your situation and current tax law.

The ITA can help you determine things like:

- Whether you need to file a tax return

- Your filing status

- Whether someone can claim you as a dependent

- If you qualify for certain tax credits

- Whether an expense is deductible

- If income is taxable

The tool is easy to use and available anytime, making it a great first stop for basic tax questions.

Keep in mind that the ITA is designed for general tax situations. If your circumstances involve a business, rental property, foreign income, retirement planning, or other complex issues, personalized tax advice is still the best option.

Questions? Let’s Talk!

Need help with a tax question the IRS tool can't answer?

We're happy to help. Contact us for a free consultation.

The article is meant for informational purposes only. Please contact me directly to discuss how this applies to your individual tax situation.

Home Sale Tax Break: Many Homeowners Can Sell Tax-Free

Selling your home can result in a substantial profit, but many homeowners are surprised to learn that they may owe no federal capital gains tax at all.

The IRS allows eligible homeowners to exclude up to:

• $250,000 of gain if filing Single

• $500,000 of gain if Married Filing Jointly

This is one of the most valuable tax breaks available, but there are several rules that must be met.

Do You Qualify?

Most homeowners qualify if they meet these requirements:

• Own the home for at least 2 years during the 5-year period before the sale.

• Live in the home as their primary residence for at least 2 years during that same 5-year period.

• Have not claimed the home sale exclusion on another home within the previous two years.

Your Gain May Be Smaller Than You Think

Your taxable gain is not simply the selling price minus the purchase price. Qualifying home improvements and certain selling expenses can reduce your taxable gain. Keep receipts for major improvements such as a new roof, kitchen remodel, room addition, or HVAC replacement.

Not Every Home Expense Counts

Routine maintenance such as painting, lawn care, cleaning, and minor repairs generally does not increase your basis or reduce taxable gain.

What If You Rented the Home?

You may still qualify for the exclusion, but depreciation claimed after May 6, 1997 generally must be recaptured, and rental or business use can complicate the calculation.

What If Your Gain Exceeds the Exclusion?

Only the amount above the $250,000/$500,000 exclusion is generally subject to capital gains tax.

Don't Forget State Taxes

Be sure to consider both federal and state tax consequences before selling your home.

Planning Before You Sell Can Pay Off

• Gather receipts for major improvements.

• Confirm you meet the ownership and residency rules.

• Review any rental or business use.

• Estimate your potential gain before closing.

How GurelCPA Can Help

At GurelCPA, we help homeowners determine whether they qualify for the home sale exclusion, calculate their adjusted basis, and estimate any tax before the sale closes. Planning ahead can make a significant difference.

The article is meant for informational purposes only. Please contact me directly to discuss how this applies to your individual tax situation.

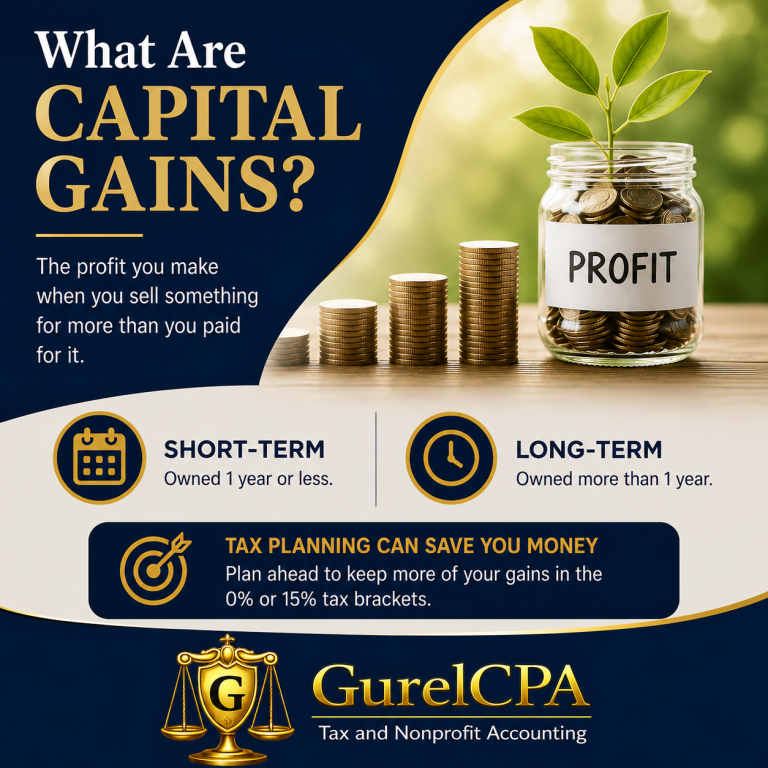

What Are Capital Gains?

When you sell something for more than you paid for it, you've earn a capital gain. Capital gains occur when you sell certain types of property, and understanding how they are taxed can help you make better financial decisions.

What Is a Capital Gain?

A capital gain is the gain you make when you sell a capital asset for more than its tax basis (usually what you paid for it, plus certain expenditures).

Short-Term vs. Long-Term Capital Gains

Short-term capital gains apply when you own an asset for one year or less before selling it and are taxed at ordinary income tax rates. Long-term capital gains apply when you own an asset for more than one year and qualify for lower tax rates. Holding an investment long enough to qualify as long-term treatment can significantly reduce the taxes owed.

Long-Term Capital Gains Have Favorable Tax Rates

For 2026, long-term capital gains are taxed at 0%, 15%, or 20%, depending on taxable income.

0% rate:

• Single: Up to $49,450

• Married Filing Jointly: Up to $98,900

15% rate:

• Single: $49,451 to $545,500

• Married Filing Jointly: $98,901 to $613,700

With a little planning, it is possible to spread gains over multiple tax years to keep more gains in the 0% bracket or avoid moving into the 20% bracket.

Tax Planning Can Reduce Capital Gains Tax

Before selling appreciated investments, real estate, or other assets, consider whether the asset has been held long enough for long-term treatment, whether the sale should occur in a lower-income year, whether multiple sales can be spread over multiple years, and whether capital losses are available to offset gains.

We're Here to Help

If you're planning to sell investments, real estate, or other appreciated assets, contact us before completing the transaction. We can help identify opportunities to minimize your capital gains tax through careful planning.

The article is meant for informational purposes only. Please contact me directly to discuss how this applies to your individual tax situation.

Hiring Seasonal or Part-Time Employees? Don't Overlook These IRS Rules

Summer often means hiring extra help. Whether you're bringing on students, temporary workers, or part-time employees, it's important to understand that these workers generally have the same federal tax requirements as full-time employees.

The IRS recently reminded employers that seasonal and part-time workers are employees for tax purposes, and employers must follow the same payroll tax rules that apply to any other employee.

Four Things Every Employer Should Know

1. Have Every Employee Complete Form W-4

All new employees should complete Form W-4 so you can withhold the correct amount of federal income tax from their wages.

2. Withhold and Pay Payroll Taxes

Seasonal and part-time employees are generally subject to the same federal income tax withholding, Social Security tax, and Medicare tax. Don't assume that working only a few months changes these requirements.

3. Classify Workers Correctly

A temporary employee is not automatically an independent contractor. If you control how, when, and where the work is performed, the worker is generally an employee. Misclassifying workers can result in significant IRS penalties.

4. Seasonal Employers May Have Different Form 941 Filing Requirements

Businesses that only operate during certain times of the year may not need to file quarterly payroll tax returns during quarters when no wages are paid. Employers should indicate that they are seasonal employers when filing Form 941 so the IRS knows returns may not be required every quarter.

Don't Let Temporary Employees Create Permanent Tax Problems

Hiring extra help can be great for your business, but payroll mistakes can become expensive. Setting up payroll correctly from the beginning helps avoid notices, penalties, and unnecessary headaches later.

The article is meant for informational purposes only. Please contact me directly to discuss how this applies to your individual tax situation.

Now You Can Download Proof of Your EIN

For years, if a business lost its original IRS EIN confirmation letter, replacing it could be a frustrating process. Many business owners had to call the IRS, wait on hold, and request a replacement Letter 147C by mail or fax.

Fortunately, the IRS has made this much easier.

Businesses that have access to an IRS Business Tax Account can now download an official digital CP575 notice confirming their Employer Identification Number (EIN). Even better, the IRS states that this digital notice may be used in place of both the original CP575 notice and Letter 147C.

Why This Matters

- Opening a business bank account

- Applying for financing

- Setting up payroll

- Working with vendors

- Completing government paperwork

- Verifying your business with financial institutions

Instead of searching through old files or contacting the IRS for a replacement, many businesses can now simply sign into their Business Tax Account and download the document immediately.

Who Can Use This Feature?

The IRS continues expanding Business Tax Account access to more types of businesses and tax-exempt organizations. Eligibility depends on your entity type and your role within the organization, but many corporations, partnerships, nonprofits, and other entities can now use these online services.

Our Recommendation

If your business doesn't already have an IRS Business Tax Account, now is a great time to create one. In addition to downloading your EIN confirmation, the account provides access to tax records, notices, payments, balances, and other useful IRS services—all without waiting on hold.

Need help setting up your IRS Business Tax Account or determining who should be registered as your Designated Official? GurelCPA can help. Contact us today to get started.

The article is meant for informational purposes only. Please contact me directly to discuss how this applies to your individual tax situation.

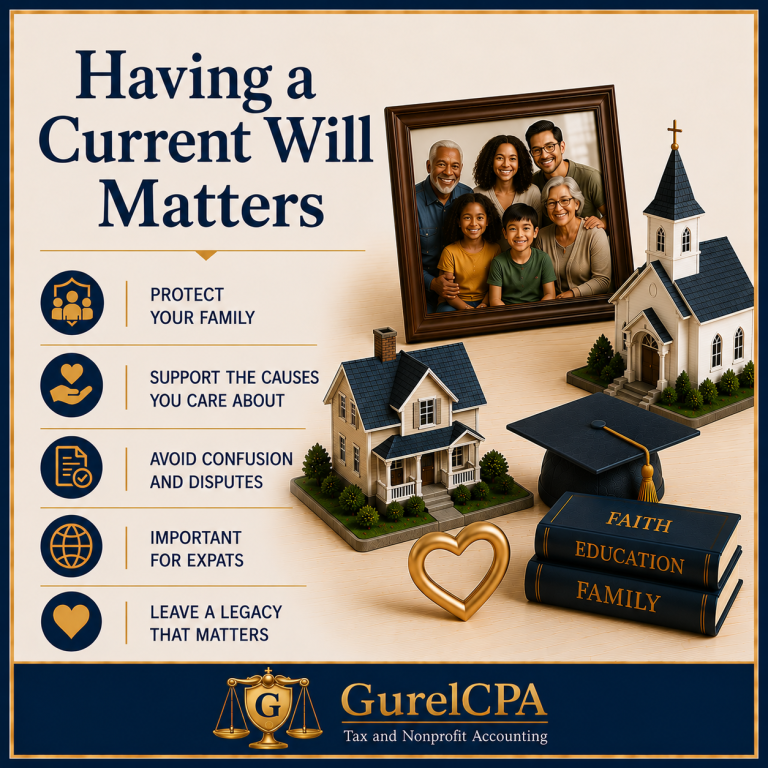

Having a Current Will Matters More Than You Think

Most people know they should have a will. Unfortunately, many people postpone creating one because they assume they are too young, do not have enough assets, or believe their family will simply work things out if something happens.

The reality is that a will is one of the most important legal and financial documents you can have. Whether you are raising a family, living overseas, running a business, supporting charitable causes, or simply trying to make life easier for your loved ones, a properly prepared will can provide clarity, reduce costs, and help prevent unnecessary disputes.

What Happens If You Die Without a Will?

When someone dies without a valid will, they are considered to have died 'intestate.' In that situation, state law determines who receives their assets and who is responsible for administering the estate.

Many people are surprised to learn that the state's distribution rules may not match their wishes.

For example:

• Unmarried partners may receive nothing.

• Stepchildren may receive nothing.

• Specific charitable gifts cannot be honored.

• Family members may disagree about who should manage the estate.

• The court may appoint someone to handle matters who would not have been your first choice.

Having a will allows you to make these decisions yourself rather than leaving them to state law.

A Will Is About More Than Money

A will can name beneficiaries, designate an executor, specify guardians for minor children, direct gifts to charities and nonprofit organizations, provide instructions regarding personal property and family heirlooms, and help reduce confusion and conflict among surviving family members.

Special Considerations for Americans Living Abroad

Expats often own assets in multiple countries, including U.S. bank and investment accounts, foreign bank accounts, foreign real estate, retirement accounts, and business interests.

Different countries may have different inheritance laws, probate procedures, and rules regarding the recognition of foreign wills. Americans living abroad should work with qualified legal professionals familiar with both U.S. and local laws to ensure their estate plan functions as intended.

Supporting Causes That Matter

Many nonprofit supporters spend years donating their time, talent, and financial resources to organizations they care about. A will allows individuals to continue supporting those causes after their lifetime through charitable bequests and other planned gifts.

The Importance of Updating Your Will

Major life events such as marriage, divorce, birth or adoption of children, death of a beneficiary or executor, significant changes in assets, or moving to another state or country should trigger a review of your estate plan.

Estate Planning Is an Act of Care

A properly prepared will can help reduce uncertainty, minimize family conflict, support charitable goals, and provide clear instructions when your loved ones need them most.

Final Thoughts

A will is one of the simplest and most effective tools available to protect your family, support your charitable interests, and ensure your wishes are carried out. Whether you live in the United States or abroad, taking the time to establish or update a will can provide valuable peace of mind.

Have questions about how estate planning decisions may affect your taxes, charitable giving, or overall financial situation? Contact Lance W. Gurel, CPA, for a free consultation.

This article is intended for informational purposes only and does not constitute legal or tax advice. Estate planning documents should be prepared with the assistance of a qualified attorney familiar with your individual circumstances.

Nonprofits: You Can Use the IRS Business Tax Account Too

Many nonprofits assume IRS online tools are only for for-profit businesses. That’s no longer the case. The Internal Revenue Service now offers a Business Tax Account (BTA) and nonprofits are included.

If your organization has an EIN and files with the IRS (Form 990, 990-EZ, or payroll returns), this is a tool you should know about.

What Is the IRS Business Tax Account?

The IRS Business Tax Account is a secure online portal that lets your organization view and manage its federal tax information in one place.

Think of it as your nonprofit’s IRS dashboard, payment center, and compliance tool.

Yes — This Applies to Nonprofits

If your organization has an EIN, files Form 990 (or 990-EZ / 990-N), or handles payroll or other federal filings, you may be able to use this system.

This is not just for businesses—it applies to nonprofits too.

What Can Your Nonprofit Do With It?

View balances and payments: See what you owe and confirm payments were applied correctly.

Make and schedule payments: Pay payroll taxes or other liabilities without mailing checks.

Access IRS records: Download transcripts and account history for lenders or grantors.

View IRS notices online: Avoid missed or delayed mail.

Manage access: Add or remove users and improve internal controls.

Why This Matters

Fewer surprises from missed notices or unknown balances.

Stronger internal controls with managed access.

Better grant readiness with organized IRS records.

Bottom Line

The IRS Business Tax Account is becoming an important tool for nonprofits. It provides better visibility, more control, and fewer surprises.

Questions? Let’s Talk!

If you’d like help setting this up or understanding how it applies to your nonprofit, please contact me directly. I offer a free consultation to help you evaluate your situation.

This article is for informational purposes only and should not be relied upon as tax advice. Please contact me directly to discuss how this applies to your organization’s specific situation.

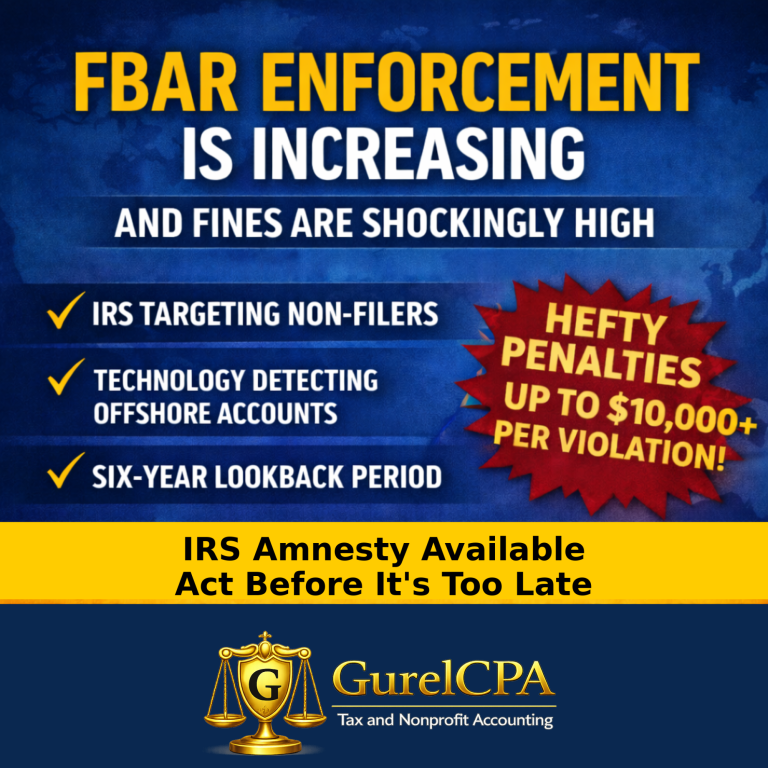

A Penalty-Free Path for U.S. Expats to Make-up Missed Tax Filings

Many U.S. citizens living abroad are surprised when they learn that they are still required to file U.S. tax returns and report certain foreign accounts — even if they owe little or no U.S. tax. They don’t realize the rule is that US citizens must report on their worldwide income and bank accounts.

If you are behind on U.S. filings, the IRS Streamlined Foreign Offshore Procedures (SFOP) may allow you to catch up without penalties, as long as your noncompliance was non-willful.

What Are the Streamlined Foreign Offshore Procedures?

The SFOP is an IRS program that allows eligible U.S. taxpayers living outside the United States to become compliant by filing overdue tax returns and submitting Foreign Bank Account Reports when required.

When done correctly, no IRS penalties are assessed, and, most filers are able to use provisions such as the Foreign Earned Income Exclusion or Foreign Tax Credit to reduce or eliminate U.S. tax owed.

Who Qualifies?

SFOP is designed for U.S. taxpayers who:

• Lived outside the U.S. during the required filing years

• Failed to file U.S. returns or international forms

• Did not willfully avoid U.S. tax obligations

This applies to both temporary and long-term residents abroad.

What Must Be Filed?

To complete SFOP, taxpayers generally submit:

• Three years of U.S. income tax returns

• Six years of foreign account reports (FBARs)

Are There Penalties?

For taxpayers qualifying under the foreign streamlined procedures:

• No late-filing penalties

• No FBAR penalties

• No accuracy-related penalties

Only actual tax due (if any) and interest must be paid.

Why Professional Review Matters

If you are a U.S. taxpayer living abroad and want to understand your options, I invite you to contact me directly. I offer a free initial consultation to review your situation and discuss next steps.

This article is for general informational purposes only and does not constitute tax advice. Every tax situation is different, and eligibility for the Streamlined Foreign Offshore Procedures depends on specific facts and circumstances.

IRS Business Tax Account: What It Is and Why Every Business Should Use It

If you own a business, the IRS has quietly rolled out one of the most important tools in years: the IRS Business Tax Account.

This isn’t just another IRS webpage; it’s a secure online portal that gives you direct access to your business tax information. For many business owners, it can replace hours of phone calls, paperwork, and guesswork.

Let’s break down what it is, what it does, and why you should care.

What Is the IRS Business Tax Account?

The IRS Business Tax Account (BTA) is a self-service online platform that allows business owners and authorized users to view and manage their federal tax information in one place.

Think of it as your business’s IRS dashboard: similar to online banking, but for taxes.

What Can You Do With a Business Tax Account?

1. View Your Balance and Payment History – See what you owe, track payments, and monitor outstanding liabilities in real time.

2. Make and Manage Payments – Make federal tax deposits, pay balances, schedule future payments, and cancel payments all in one place.

3. Access Tax Records and Transcripts – Download tax return transcripts, account transcripts, and compliance reports.

4. Read IRS Notices Online – View IRS notices digitally and track correspondence without waiting for mail.

5. Manage Who Has Access – Add or remove authorized users and control access levels to your business tax data.

6. Approve Third-Party Requests – Approve or reject lender requests for tax information directly inside your account.

Why This Matters

Faster answers, better financial control, fewer surprises, and alignment with the IRS’s ongoing shift toward digital systems.

Important Limitations

The system is still evolving, and access varies depending on your business structure and role.

Bottom Line

The IRS Business Tax Account is becoming an essential tool for business owners, offering real-time visibility and improved control.

Questions? Let’s Talk!

If you’d like help setting up your IRS Business Tax Account or understanding how to use it effectively, please contact me directly. I offer a free consultation to get you started.

This article is for informational purposes only and should not be relied upon as tax advice. Please contact me directly to discuss how this applies to your individual tax situation.

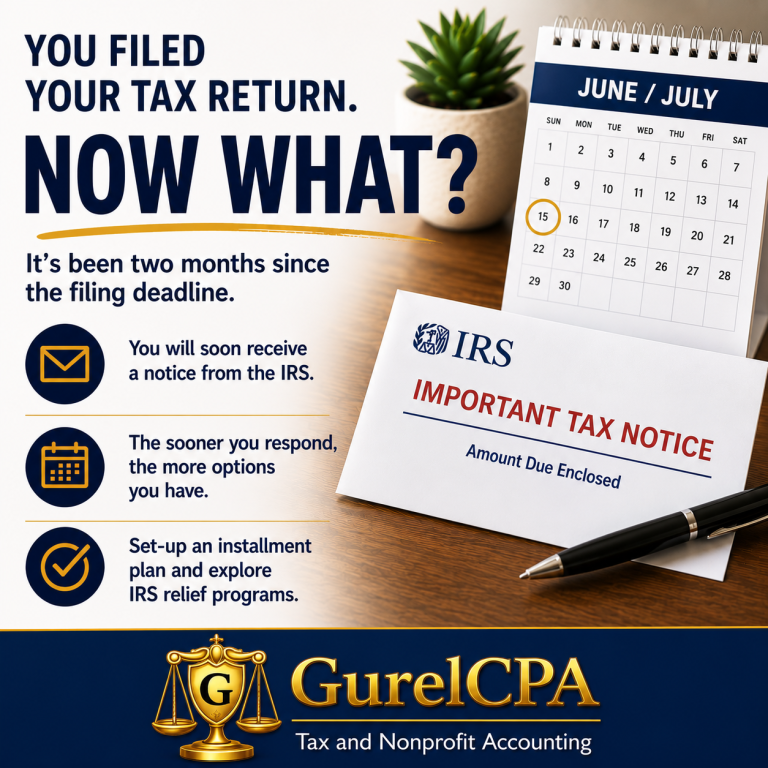

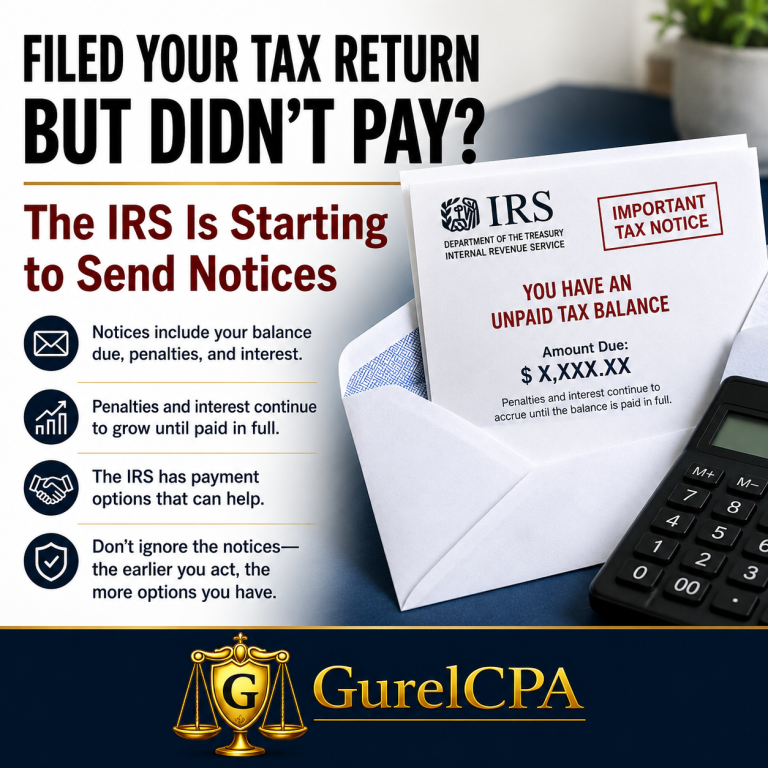

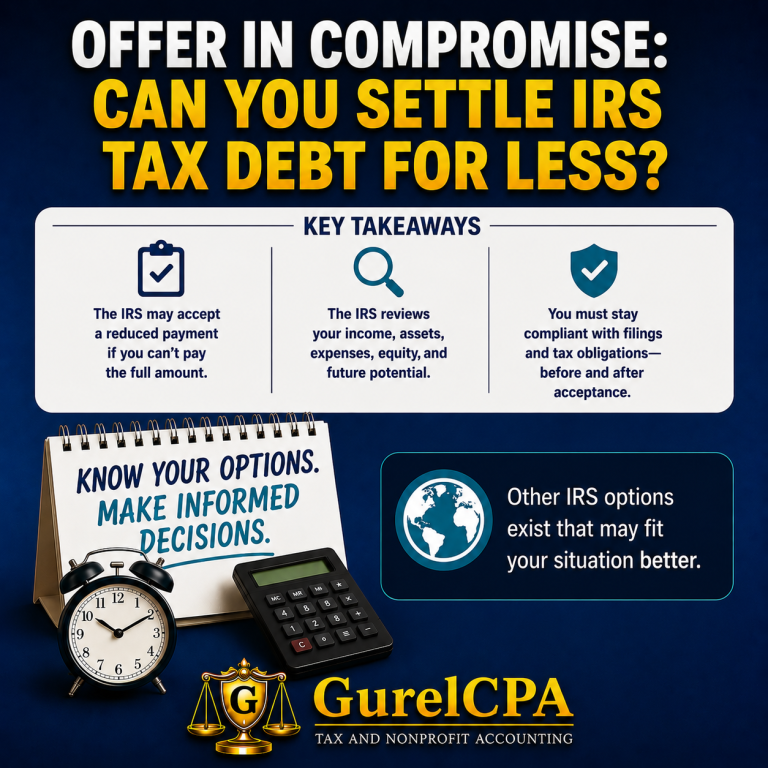

You Filed Your Tax Return But Didn’t Pay: What Happens Next?

If you filed your tax return but couldn't afford to pay the balance due, you did the right thing by filing on time.

Now comes the next step.

About two months after tax season, many taxpayers begin receiving IRS balance-due notices in the mail. The most common is Notice CP14, which tells you how much you owe, including penalties and interest. For many people, opening that letter can be stressful. But receiving a balance-due notice is often the best time to take action.

First, don't ignore the notice. The IRS sends these notices because a tax return was filed showing a balance due that was not paid in full. If no action is taken, penalties and interest continue to accumulate, and the IRS collection process can become more serious.

Installment Agreements: The Most Common Solution

For many taxpayers, an IRS installment agreement is the simplest answer. An installment agreement allows you to make monthly payments over time rather than paying the entire balance immediately. Even if you cannot pay the full amount today, paying something and establishing a payment plan is often far better than doing nothing.

What If You Truly Can't Afford Payments?

If your financial situation is severe, the IRS has other programs that may help.

Currently Not Collectible Status

Taxpayers experiencing genuine financial hardship may qualify for a temporary suspension of collection activity. This doesn't erase the debt, but it can provide breathing room while you get back on your feet.

Offer in Compromise

In some situations, taxpayers may be able to settle their tax debt for less than the full amount owed. While not everyone qualifies, it can be a valuable option for taxpayers facing long-term financial hardship.

Make Sure the Notice Is Correct

Before paying, review the notice carefully. Occasionally taxpayers receive a balance-due notice after they have already paid, particularly when payments are still being processed or posted to the IRS account.

The Bottom Line

Filing your return was the first step. Now it's time to deal with the balance due.

The good news is that the IRS would much rather work with taxpayers who communicate and make arrangements than with those who ignore the problem.

If you've received an IRS balance-due notice and aren't sure whether an installment agreement, Offer in Compromise, or another relief option is right for you, contact me for a free consultation. Together we can review your situation and determine the best path forward.

The article is meant for informational purposes only. Please contact me directly to discuss how this applies to your individual tax situation.

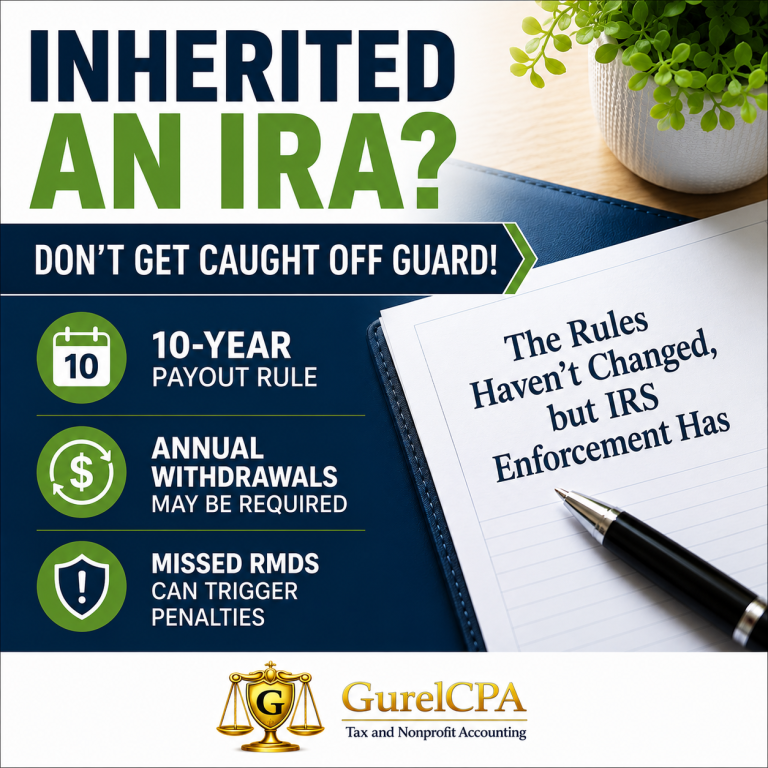

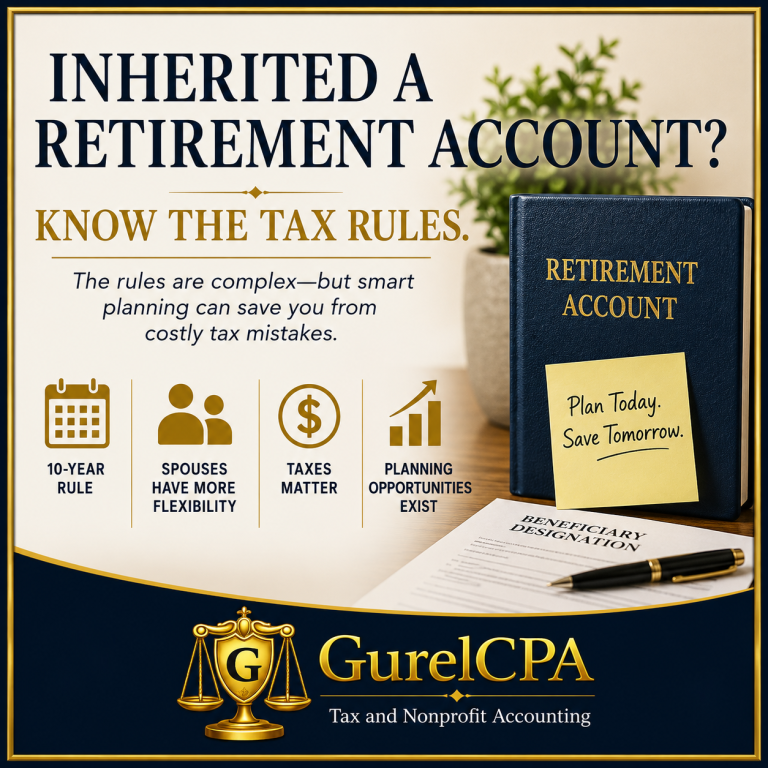

Inherited an IRA? The IRS Is Enforcing These Required Minimum Distribution Rules

If you've been seeing articles about Required Minimum Distributions (RMDs) lately, you may be wondering whether the rules changed again.

For most retirees, the answer is no.

The age for starting RMDs remains 73 for individuals born between 1951 and 1959, and 75 for those born in 1960 or later. If you're already taking RMDs from your retirement accounts, there is probably nothing new to worry about.

The real story involves inherited IRAs.

The Surprise for Many IRA Beneficiaries

Under the SECURE Act, most non-spouse beneficiaries who inherit an IRA must withdraw the entire account within 10 years. For several years, however, the IRS delayed enforcement while it finalized the regulations.

Now those regulations are in place, and many beneficiaries are discovering that the 10-year rule may not work the way they expected.

If the original IRA owner had already begun taking RMDs before passing away, many beneficiaries must:

• Take annual distributions during years 1 through 9, and

• Completely empty the account by the end of year 10.

Many taxpayers believed they could simply wait until year ten and withdraw the entire balance. In many cases, that is no longer allowed.

Penalties Are Smaller, but Still Expensive

The SECURE 2.0 Act reduced the penalty for missed RMDs.

The old penalty was 50% of the amount that should have been withdrawn. Today, the penalty is generally 25%, and it may be reduced further if corrected quickly.

That's certainly better than before, but it can still be a costly mistake.

Why This Matters

Many inherited IRA beneficiaries have never taken a required distribution because the IRS repeatedly postponed enforcement of these rules.

Now that enforcement has begun, beneficiaries who miss required withdrawals could face penalties and unexpected tax issues.

There is also a planning opportunity. Taking distributions strategically over several years may help reduce the tax impact compared to waiting and taking large withdrawals later.

The Bottom Line

Most retirees don't need to worry about new RMD rules this year.

However, if you inherited an IRA after 2019, it may be time to take a closer look. The IRS is now enforcing inherited IRA distribution requirements that many beneficiaries have never had to follow before.

If you're unsure whether an inherited IRA requires an RMD this year, don't guess. A quick review now could prevent penalties and help you avoid unnecessary taxes later.

Questions about inherited IRAs, retirement distributions, or tax planning? Contact GurelCPA for a free consultation. We're happy to help you understand your options and stay compliant with the IRS.

This article is meant for informational purposes only and should not be relied upon as tax or legal advice. Please contact Lance W. Gurel, CPA directly to discuss your individual tax situation and inherited retirement account planning opportunities. Free consultations are available.

Just Married? It's a Good Time to Check Your Tax Withholding

Wedding planning usually focuses on venues, flowers, travel, and thank-you notes. Taxes rarely make the list.

But if you recently got married, one of the smartest financial moves you can make is reviewing your tax withholding.

A change in marital status can affect how much tax should be withheld from your paycheck, and failing to update your withholding could lead to an unexpected tax bill, or a larger refund than necessary, when you file your return.

Why Marriage Can Change Your Tax Situation

For federal tax purposes, if you are married on December 31, the IRS generally considers you married for the entire year. That means you'll typically file either Married Filing Jointly or Married Filing Separately.

Many couples benefit from filing jointly, but the amount of tax withheld from their paychecks may need adjustment, especially when both spouses work.

Update Your Form W-4

The IRS recommends that newly married couples review and update their Form W-4 with their employers.

Use the IRS Tax Withholding Estimator

The IRS Tax Withholding Estimator can help determine whether your withholding is on track by considering filing status, income, credits, deductions, and other factors.

Don't Forget to Update Social Security Records

If either spouse changes their name after marriage, updating records with the Social Security Administration should be a top priority.

The IRS matches the name and Social Security number shown on a tax return against SSA records.

If the name on the tax return does not match the name on file with Social Security, the return may be rejected when electronically filed or processing may be delayed.

Other Important Tax Updates for Newlyweds

Marriage often brings other changes that can affect your tax return, including updating addresses, reviewing beneficiary designations, evaluating filing status options, and adjusting estimated tax payments if needed.

The Bottom Line

Taking a few minutes now to update your W-4, verify your withholding, and ensure your Social Security records are current can help prevent surprises and filing problems next tax season.

If you've recently married and would like help reviewing your withholding, filing status options, or overall tax situation, contact GurelCPA. We offer a free initial consultation and would be happy to help.

The article is meant for informational purposes only. Please contact me directly to discuss how this applies to your individual tax situation.

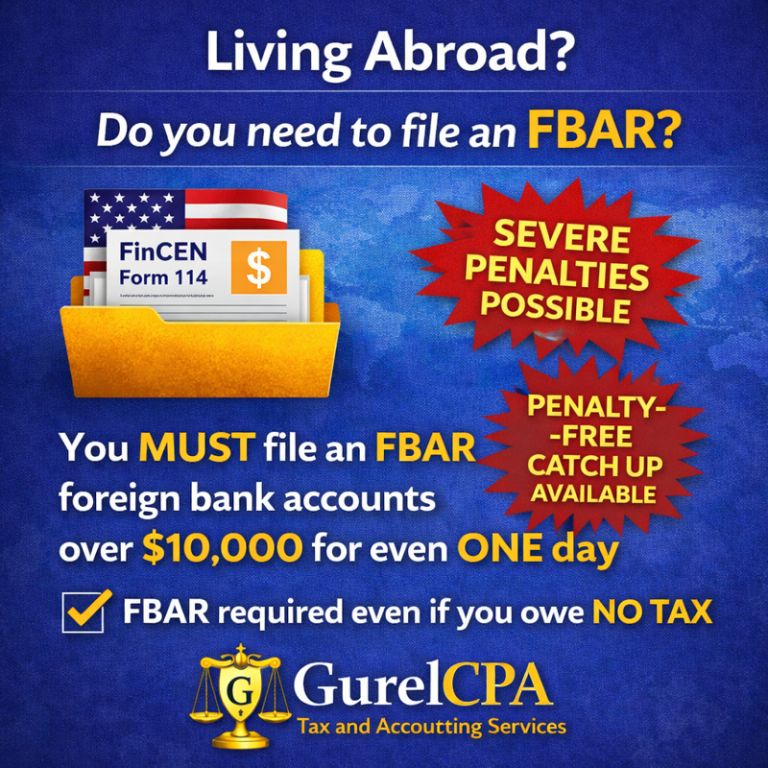

Living Abroad? Do you need to file an FBAR?

Many U.S. citizens living outside the United States are surprised to learn that filing a tax return may not be their only reporting obligation. In addition to your federal income tax return, you may also need to file something called an FBAR.

You must file an FBAR if the combined total of your foreign financial accounts exceeded $10,000 at any time during the year.

What Is an FBAR?

FBAR stands for Foreign Bank Account Report. The official name is FinCEN Form 114, and it is filed electronically with the U.S. Treasury, not with your tax return.

It does not matter if:

• The balance only exceeded $10,000 for one day

• The funds were already taxed in another country

• You owe no U.S. income tax

If the threshold is met, the reporting requirement applies.

What Accounts Count?

Foreign financial accounts may include:

• Foreign checking and savings accounts

• Foreign investment or brokerage accounts

• Some foreign retirement accounts

• Joint accounts

• Accounts where you have signature authority

If the account is located outside the United States, it may be reportable.

Important: It’s $10,000 Combined

The $10,000 threshold applies to the total of all foreign accounts combined, not per account. If your combined balance exceeds $10,000 at any point during the year, an FBAR is generally required.

Is an FBAR a Tax?

No. The FBAR does not calculate tax and does not create tax by itself. It is strictly an informational reporting requirement.

Many expats owe little or no U.S. income tax because of the Foreign Earned Income Exclusion or Foreign Tax Credit, but the reporting obligation may still exist.

What If You Didn’t Know?

Many expats miss FBAR filings simply because they were unaware of the rule. If the failure to file was non-willful, there are compliance options available to correct past years without penalties

The Bottom Line

If you are a U.S. citizen or green card holder living abroad, it is important to determine whether FBAR reporting applies to you. If you are a U.S. taxpayer living abroad and are unsure whether you should be filing FBARs, or whether you may need to correct past filings, I invite you to contact me directly for a free initial consultation to review your situation and discuss your options.

This article is for general informational purposes only and does not constitute tax advice. FBAR requirements depend on individual facts and circumstances

IRS Identity Protection PIN: A Simple Tool to Help Prevent Tax Fraud

Identity theft continues to be one of the most common tax-related problems facing taxpayers. Criminals often use stolen personal information to file fraudulent tax returns and claim refunds before the legitimate taxpayer has a chance to file.

One of the simplest ways to help protect yourself is by obtaining an IRS Identity Protection Personal Identification Number, commonly called an IP PIN.

What Is an IP PIN?

An IP PIN is a six-digit number issued by the IRS that helps verify your identity when you file your federal tax return. Once an IP PIN is assigned to your Social Security Number, the IRS generally will not process an electronically filed tax return without the correct PIN.

Why Does It Matter?

If someone obtains your Social Security Number, they may attempt to file a fraudulent tax return and claim a refund in your name. An IP PIN helps prevent this because the fraudster would also need your current year's PIN in order to successfully file.

Who Should Consider Getting One?

An IP PIN may be especially worth considering if you:

• Have been a victim of identity theft in the past

• Have had personal information exposed in a data breach

• Want an additional layer of protection for your tax return

• Are concerned about increasing online fraud and scams

Things to Know Before You Enroll

• A new IP PIN is issued each year.

• You must use the current year's PIN when filing.

• Keep it in a safe place.

• Losing your IP PIN can delay the filing process.

• The IP PIN applies to federal tax returns.

Is an IP PIN Right for You?

For many taxpayers, obtaining an IP PIN is a simple and effective way to add another layer of security to their tax filing process. While no system can eliminate fraud entirely, an IP PIN can make it significantly more difficult for criminals to file a fraudulent tax return using your information.

Need Help?

Questions about IRS identity theft protection, tax account security, or other IRS tools? Contact me directly for a free consultation.