Understanding 529 Plans: A Smart Way to Save for Education

What Is a 529 Plan?

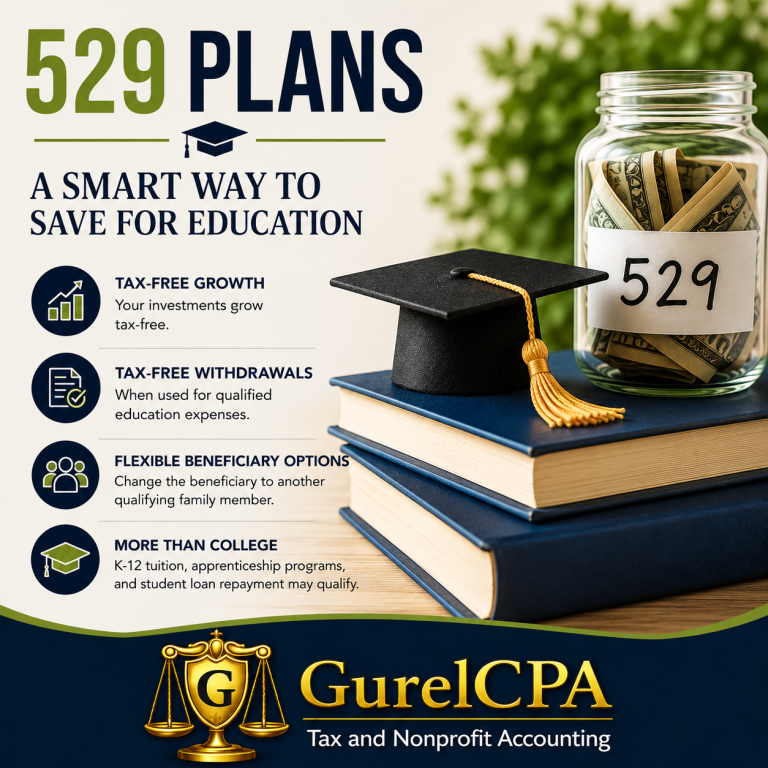

A 529 plan is a state-sponsored savings plan designed to encourage saving for education expenses. Contributions are made with after-tax dollars, but the earnings grow tax-free, and qualified withdrawals are also tax-free.

The beneficiary can be a child, grandchild, spouse, or even yourself.

Tax Benefits of a 529 Plan

The primary tax advantages include:

• Tax-free growth on investments within the account.

• Tax-free withdrawals when used for qualified education expenses.

• Potential state tax deductions or credits, depending on the state sponsoring the plan.

• No federal income tax deduction for contributions.

For many families, years of tax-free growth can result in significant savings compared to investing in a taxable account.

What Expenses Qualify?

College and University Expenses

• Tuition and fees

• Books and supplies

• Computers and related equipment

• Room and board (for eligible students)

K–12 Education

• Up to $10,000 per year may be used for tuition at public, private, or religious elementary and secondary schools.

Apprenticeship Programs

• Qualified apprenticeship expenses may qualify if the program is registered with the U.S. Department of Labor.

Student Loan Repayment

• Up to $10,000 may be used toward the beneficiary's student loans, with certain limitations.

What Happens If the Child Doesn't Go to College?

Fortunately, the account owner has options:

• Change the beneficiary to another qualifying family member.

• Keep the funds invested for future educational needs.

• Use the funds for another child's education.

• Withdraw the funds (earnings may be subject to income tax and penalties if not used for qualified expenses).

Recent law changes have also created opportunities to roll certain unused 529 funds into a Roth IRA for the beneficiary, subject to several requirements and annual contribution limits.

Who Controls the Money?

The person who establishes the account remains in control of the funds. The beneficiary does not automatically gain ownership when reaching adulthood.

This allows parents and grandparents to maintain flexibility and ensure the funds are used as intended.

Contribution Limits

529 plans generally have very high lifetime contribution limits, often exceeding $300,000 per beneficiary depending on the state plan.

Contributions may also qualify for special gift-tax averaging rules, allowing larger amounts to be contributed without triggering federal gift tax concerns.

Choosing a 529 Plan

You are not required to use your own state's plan. Many investors compare plans based on:

• Investment options

• Fees and expenses

• State tax benefits

• Historical performance

• Ease of use

The best choice depends on your family's goals and circumstances.

.

The Bottom Line

A 529 plan can be one of the most effective tools available for education savings. Tax-free growth, tax-free qualified withdrawals, and flexible beneficiary rules make these plans attractive for many families.

Starting early allows investments more time to grow and may significantly reduce the financial burden of future education costs.

If you have questions about 529 plans, education tax credits, gift tax implications, or education funding strategies, please contact GurelCPA for a free consultation.

The article is meant for informational purposes only. Please contact me directly to discuss how this applies to your individual tax situation.